Newsletters

Newsletters

U.S.-based S&P Global raised Türkiye’s 2026 average inflation forecast to 28.9% from 23.4%, citing renewed price pressures from rising energy costs amid the Iran war in its latest emerging markets outlook report.

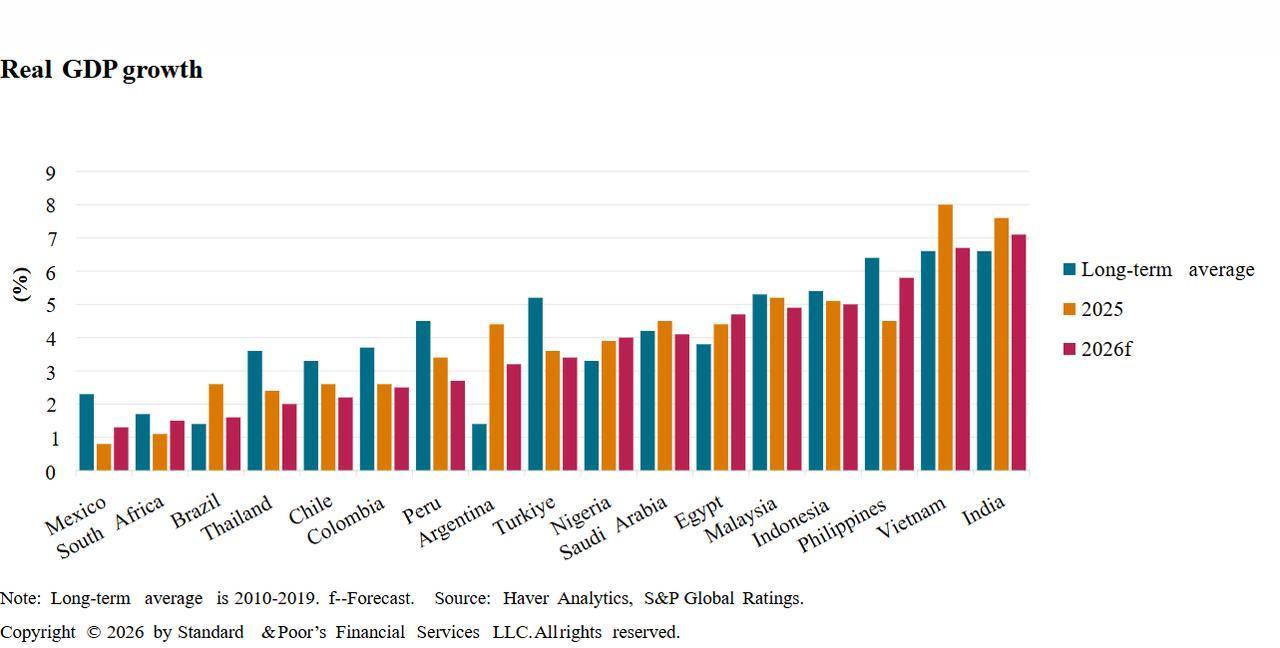

Inflation is expected to ease gradually, falling to 18.4% in 2027, 13.7% in 2028, and 12.7% in 2029, while policy rates are seen declining to 32.5% in 2026, 25.0% in 2027, and 12.5% by 2028–2029. Despite tight policy, growth is projected to hold up at 3.4% in 2026, slightly below 3.6% in 2025, supported by agriculture, gold-driven household wealth, and credit momentum.

As of February, Türkiye’s inflation accelerated to 31.5% on the back of weather-driven food supply shocks, while the Central Bank of the Republic of Türkiye (CBRT) effectively raised its funding cost to 40% after the war began and paused its easing cycle in mid-March, holding the policy rate at 37%.

The report said its baseline scenario assumes the Middle East war continues into early April, with the impact on energy prices and financial conditions remaining temporary. However, it warned that risks are skewed to the downside and depend on how the conflict evolves.

A longer or more severe conflict could drive inflation higher, push up interest rates, and weigh on growth across most emerging markets, especially in energy-importing economies and those directly exposed to the region. Energy markets are seen as the main transmission channel, as higher oil and gas costs feed into broader prices through transport, fertilizers, and industrial production, while also tightening financial conditions.

S&P Global noted that while oil markets started from a relatively well-supplied position, the risk of physical shortages would increase if the conflict persists, potentially pushing prices higher. In its baseline scenario, Brent crude is expected to average $80 per barrel this year and $65 in 2027, assuming initial price pressures ease.

Despite these risks, revisions to growth projections remain limited. Real GDP across emerging markets (excluding China) is expected to slow to 4.5% in 2026 from 4.9% in 2025, as stronger-than-expected activity in late 2025 partly offsets the impact of higher energy prices. Regional trends vary, with Asia benefiting from resilient demand and technology exports, while revisions in other regions remain mixed.

The report added that central banks, which had been moving toward rate cuts, may delay easing or tighten policy to keep inflation expectations in check.

Higher interest rates could tighten financial conditions further, while a shift by investors toward safe-haven assets could lead to additional currency depreciation, adding to inflationary and borrowing pressures across emerging markets.

1 min read

1 min read

1 min read

1 min read