Newsletters

Newsletters

The fertilizer cooperative in Muzaffarnagar, Uttar Pradesh, is quiet, although it is almost April. There are no queues. Everything looks fine.

And that’s a problem.

India stands on the cusp of a new financial year, as the Gulf is, if not on fire, smouldering. This matters here in ways that haven't quite landed yet because the "rabi" (winter) crops of wheat, barley, peas, and gram are nearly in. The fields look fine. Nobody at the farm gate is screaming.

The screaming, if it comes, arrives later.

India has seen what a bad July looks like.

Last "kharif" (monsoon planting) season, women in Haryana were marking spots in fertilizer queues overnight—bags and clothing laid out on the ground before the sun came up—only to leave empty-handed when the distribution centers ran dry.

Tamil Nadu's chief minister wrote directly to the Indian Prime Minister Narendra Modi.

Karnataka got roughly half its diammonium phosphate (DAP) allocation and called it a crisis.

By August, it had fallen to 3.7 million tonnes from 8.6 million tonnes the previous year. The government called it adequate. Farmers called it something else.

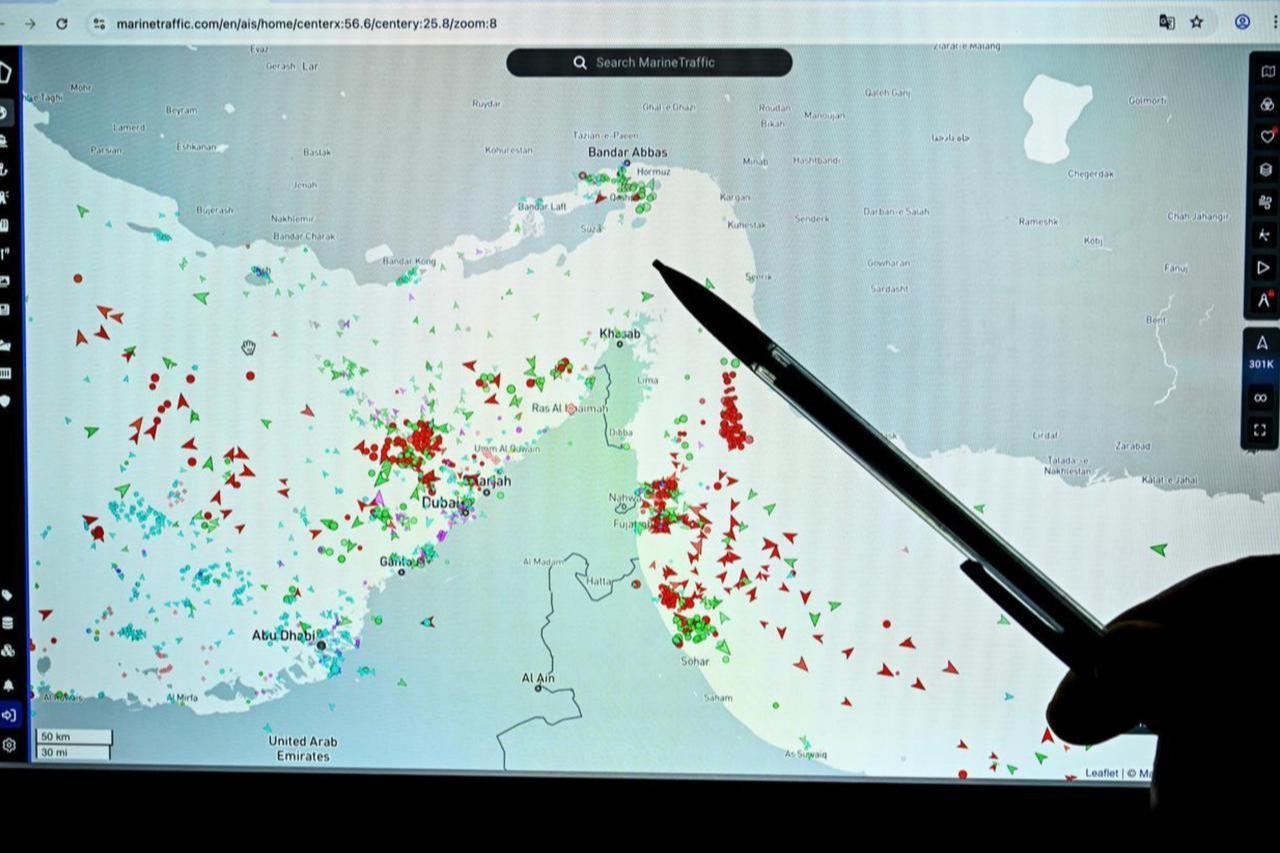

And that was before hostilities blocked the Strait of Hormuz.

Since the war began, only 21 tankers have transited the Strait of Hormuz, which typically carries 20-30% of the global urea trade. It is a choke point that accounts for 40% of India’s fertilizer imports.

It was a reality Modi acknowledged in the Lok Sabha three weeks later. By then, New Delhi had quietly ordered 1.4 million tonnes of urea from abroad and invoked the Essential Commodities Act to ration the gas that domestic plants run on.

The buffer is exceptionally thin. India currently holds roughly 6.2 million tonnes of urea against an annual consumption of 40 million tonnes, representing a reserve of just eight weeks.

"July and August are the crucial months," said Nidhi Jamwal, an agricultural journalist. In April, she noted, it is too early to comment on a shortage. The point being: by the time it isn't too early, it will be too late.

Meanwhile, March storms, including hail, have damaged parts of the winter crop. Farmers across the country are counting on monsoon planting staples, such as rice and soybeans, to make it right. A disrupted winter season plus a fertilizer-stressed monsoon planting is not a food crisis headline.

The scale of the hit is often invisible. India’s first advance estimate put the 2024–25 monsoon planting rice output at 120 million tonnes. Even a 2% hit to that crop alone would imply roughly 2.4 million tonnes lost, equivalent to the annual cereal intake of something like 20 to 25 million people, depending on the denominator used. It is a mass of people eating less well than they did last year, which won’t make the headlines.

The math is brutal: less fertilizer, lower yields, higher prices, and emptier plates. This hits people already running on cereal protein, which digests at roughly half the rate of meat or dairy, especially in states where a nutritious diet costs more than a day's wages for those breaking ground in 40-degree heat.

The government says stocks are higher than last year. One official allowed that "if the war goes on longer, things could get tight."

The numbers suggest it already is: India's urea subsidy bill was running at nearly $13 billion this year before the war started and has since proposed a further $2 billion to offset rising input costs.

Chaudhari Suresh Kumar, director general of the Fertiliser Association of India, is less guarded: the gas supply, he says, is curtailed up to 40%.

Fertilizer is made from gas. Thirty of India's 32 urea plants run on it, 60% sourced from Qatar's Ras Laffan terminal, which has reportedly been damaged. You can track where that sentence goes.

India is trying to reroute its supplies. Russia, Belarus, Morocco—anyone with urea and a ship will do.

But if the Gulf is a bottleneck of geography, Beijing is a bottleneck of intent. Export restrictions have been tightening since before the war began, and China, the world’s top urea producer, has decided that emergency shortages elsewhere sound like somebody else’s problem.

India’s DAP imports from China fell from 2.2 million tonnes in 2023–24 to 0.8 million tonnes in 2024–25. By mid-2025, Indian press reports said no fresh Chinese DAP had arrived since the start of calendar 2025.

What India receives now looks less like a renewed flow than the residue of earlier trade.

The mechanism is not a market outcome.

China's phosphate supply—the same feedstock that makes DAP—is being redirected to electric vehicle battery production. India's monsoon planting crops and China's EV sector are competing for the same molecules, administered via quarantine procedures that require no public acknowledgment. The result: cargo that might otherwise move does not.

Dr. Lorenzo Rosa, Principal Investigator at Carnegie Science, Stanford, California, calls the present disruption "potentially more severe than the 2022 shock"—the one that followed Russia's invasion of Ukraine, when markets still had room to reroute and hunt for substitutes. Now the buffers are thinner and the disruption lands in two places at once: shipping and production.

Middle East urea prices are already up 40% from pre-war levels. Nitrogen could double if the conflict extends.

At that point, the math is not about importing invoices. It's about application rates on smallholder fields in states where the memory of last season's empty cooperative shelves is still fresh.

China could soften this. It could ease restrictions and let urea move. It has given every indication it will do no such thing, making Beijing less a participant in this story than a gatekeeper.

The bomb, as it happens, is not the shortage.

It is the lag between the decision and the recognition. By July, that decision will already have been made. In a cooperative in Uttar Pradesh, a man will be running from shop to shop. The monsoon planting crop will tell you what Beijing decided in April.

2 min read

2 min read