Newsletters

Newsletters

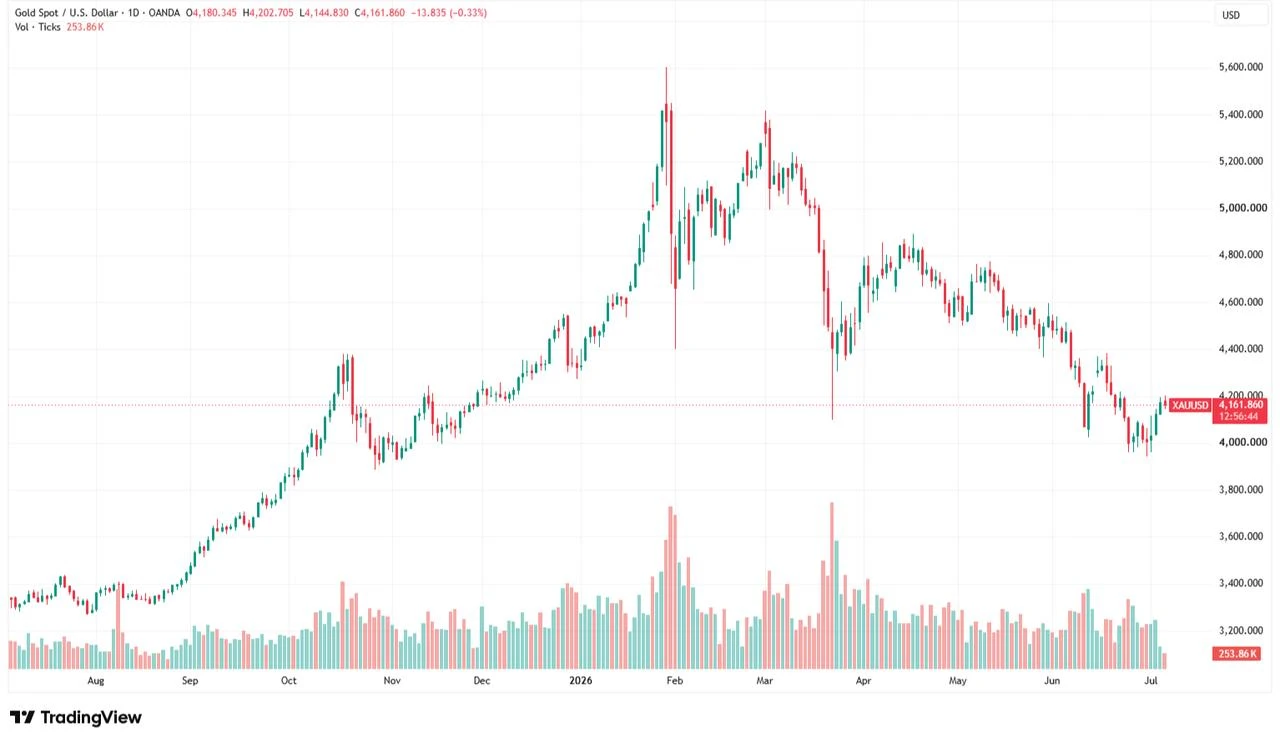

Gold prices edged lower Monday after touching a two-week high last week, while global equities showed little direction as investors weighed a firmer U.S. dollar and looked ahead to fresh clues on the Federal Reserve's interest rate path.

Spot gold slipped 0.3% to around $4,160 an ounce by 7:30 a.m. GMT after earlier reaching its highest level since June 22. U.S. gold futures for August delivery rose 1% to $4,170 an ounce after the U.S. dollar index climbed 0.2% to the 101 level.

The uncertain Fed outlook has also widened the gap between major global banks, whose forecasts for bullion now range from $4,300 to $5,200 an ounce, reflecting differing expectations for interest rates, investment flows and central bank demand.

Asian markets were largely subdued, with Japan's Nikkei 225 and China's Shanghai Composite little changed, South Korea's Kospi slipping 0.5% and Hong Kong's Hang Seng gaining 0.8%.

European stocks also lacked clear direction as the pan-European Stoxx 600 and Germany's DAX hovered around flat, while France's CAC 40 and Britain's FTSE 100 each rose 0.4%. Türkiye's BIST 100 added 0.9%, while U.S. equities traded higher, led by a 0.9% gain in the tech-heavy Nasdaq.

Elsewhere in commodity markets, silver fell 0.6% to $62 an ounce, platinum traded above $1,630, and palladium rose 0.6% to $1,260.

Oil prices also remained under pressure, with Brent crude down 0.5% at $71.8 a barrel and U.S. benchmark WTI losing 0.6% to $68.4. The losses came after OPEC+ agreed to raise its August production target by another 188,000 barrels per day, reinforcing expectations of stronger global supply as exports through the Strait of Hormuz continue to recover.

Bitcoin added 0.2% to $62,940, while ether gained 0.4% to $1,770, lifting the total cryptocurrency market capitalization to $2.2 trillion.

The latest U.S. employment report released last week showed job growth slowed sharply in June, while payroll figures for the previous two months were revised lower, reinforcing signs of a cooling labor market and prompting investors to dial back expectations for another near-term Federal Reserve rate increase.

Although the unemployment rate declined to 4.2% from 4.3% in May, the improvement largely reflected 720,000 people leaving the labor force, pushing the participation rate to its lowest level in more than five years.

Traders now see about a 54.5% chance of a September rate hike, according to the CME FedWatch Tool.

At its June 16-17 meeting, the Federal Reserve unanimously kept its benchmark interest rate unchanged at 3.50%-3.75% in the first policy decision under Chair Kevin Warsh, while signaling that further tightening remained on the table and prompting markets to raise expectations for another rate hike.

Those expectations eased after Warsh spoke at the European Central Bank's annual forum in Sintra, Portugal, on July 1. While reaffirming the Fed's commitment to its 2% inflation target and stressing that future decisions would depend on incoming data, Warsh said inflation risks had eased in recent weeks and stopped short of signaling that another rate hike was imminent.

Attention now turns to this week's Federal Open Market Committee meeting minutes, which investors hope will offer a clearer read on policymakers' thinking. Markets will watch for signs of whether more officials share Kevin Warsh's hawkish stance or whether broader support is emerging for a more dovish approach.

With markets reassessing the Fed's policy path, major investment banks remain far from a consensus on gold, reflecting differing views on how interest rates, central bank buying and investor demand will shape bullion over the coming quarters.

Goldman Sachs remains among the most bullish, seeing prices reaching $4,900 an ounce by the end of 2026 as sustained central bank purchases and reserve diversification by emerging economies continue to underpin demand.

Bank of America also expects bullion to stay elevated, putting gold at $4,800 an ounce in the fourth quarter of 2026 despite trimming its short-term outlook as softer investor demand and lingering Fed uncertainty weigh on prices.

Morgan Stanley and UBS take an even more optimistic view, both pointing to a potential climb toward $5,200 an ounce, although Morgan Stanley argues such gains would require a much stronger pickup in inflows into gold exchange-traded funds.

Not all institutions share that optimism. Deutsche Bank lowered its second-half forecast, penciling in gold at $4,300 an ounce in the third quarter before a rebound to $4,800 in the fourth as markets adjust to evolving expectations for U.S. monetary policy.

JPMorgan also turned more cautious, lowering its projections to $4,300 an ounce in the third quarter and $4,500 in the fourth while warning that resilient U.S. economic data could weigh further on bullion.

ING likewise trimmed its outlook, arguing that elevated bond yields, a stronger dollar and weaker ETF demand are likely to keep gold under pressure in the near term.

The World Gold Council, meanwhile, expects gold to remain broadly range-bound under the current economic backdrop but believes weaker growth, renewed geopolitical tensions or shifting expectations for lower interest rates could lift prices back toward $4,500 an ounce or higher.

1 min read

1 min read

1 min read

1 min read