Newsletters

Newsletters

Türkiye’s financial markets are holding relatively steady despite turbulence linked to the Iran conflict, but risks of stronger capital outflows are building, the European Bank for Reconstruction and Development (EBRD) said.

In its latest Regional Economic Update, the bank said the current sell-off wave has so far remained "manageable," while warning that pressures "may intensify" if global conditions worsen.

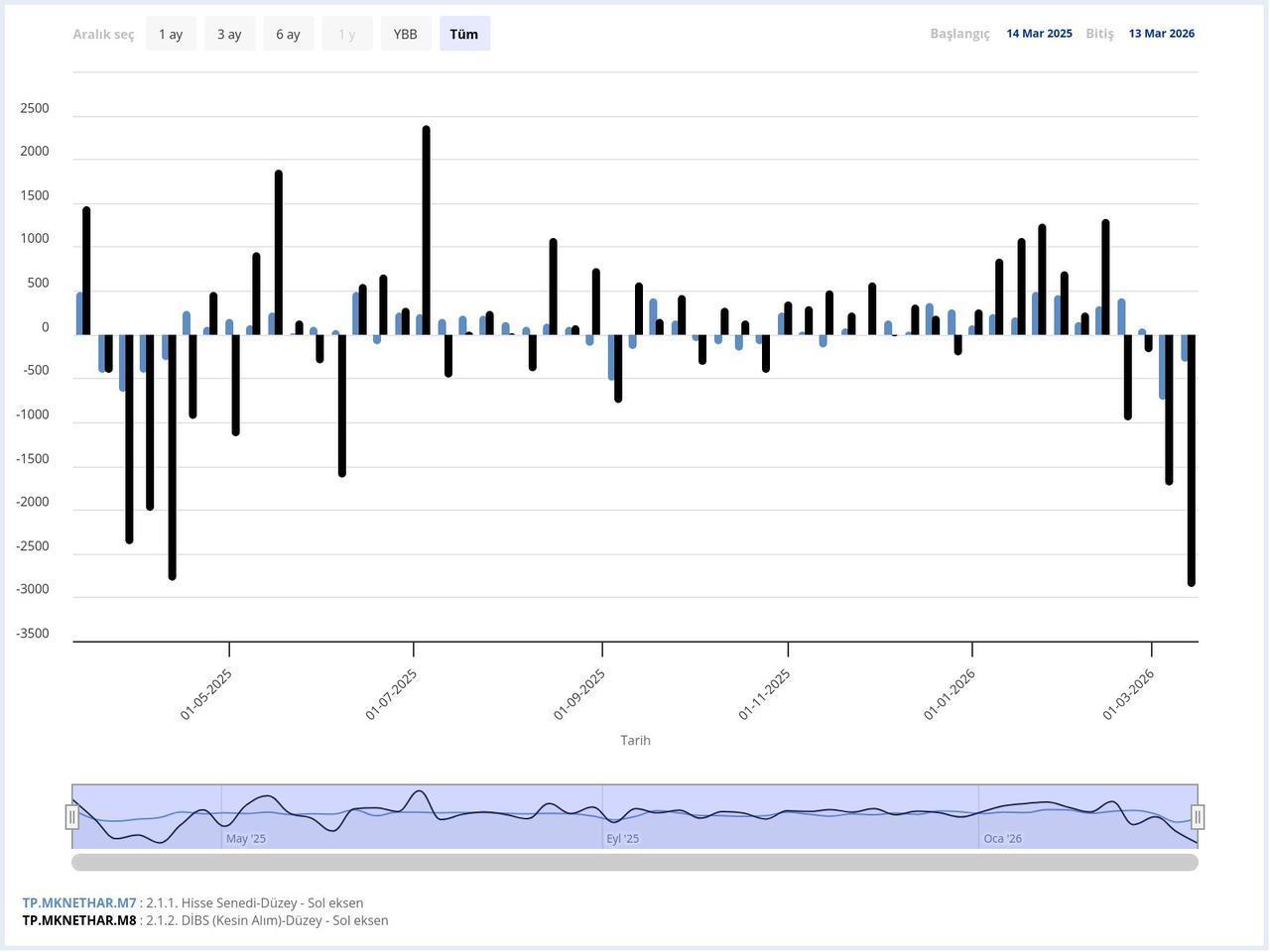

Recent central bank data already point to rising strain. Foreign investors sold a record $2.9 billion in Turkish bonds in the week of Mar. 13, bringing total net outflows to $4.6 billion. They also offloaded $322 million in equities, with stock outflows exceeding $1 billion in the first two weeks of March. Carry trade volume dropped by $12 billion, while reserves declined by nearly $25 billion over the same period.

The EBRD said borrowing costs are increasing across the southern and eastern Mediterranean, including Türkiye, as investor sentiment turns more cautious. While capital flows remain contained for now, the bank noted that prolonged geopolitical tension—particularly through energy markets—could accelerate outflows from emerging economies.

Beyond financial channels, supply-side risks are also building. Disruptions to fertiliser shipments through the Strait of Hormuz, which handles around 25%–35% of global supply, are emerging as another pressure point. Türkiye sources 13% of its fertiliser imports from Gulf Cooperation Council countries, leaving it exposed to the bottleneck and adding to inflation alongside rising energy costs, the report said.

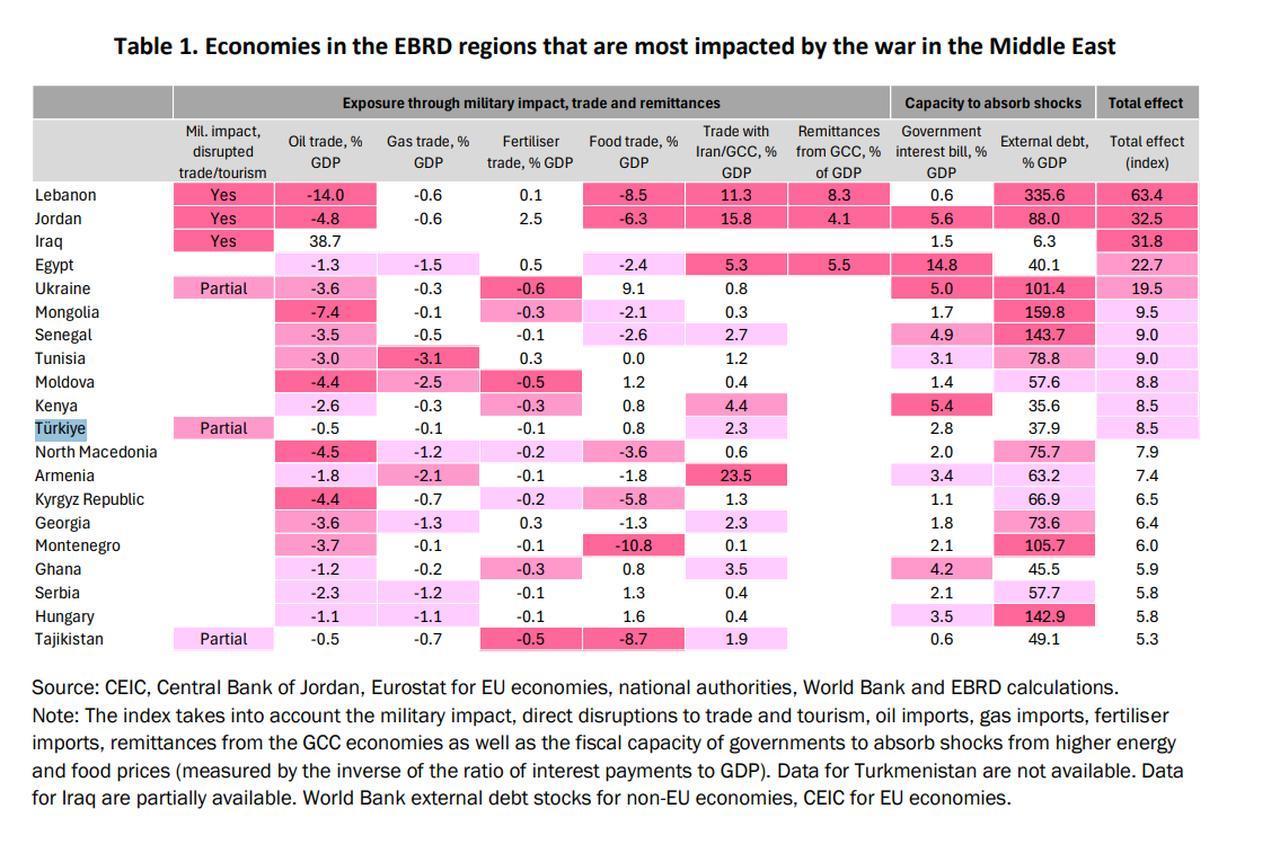

Overall, Türkiye is classified among moderately affected economies, with an impact score of 8.5. Its exposure is driven mainly by financial channels, trade ties with Gulf countries and Iran, and sensitivity to remittance flows. However, relatively lower external debt and a manageable government interest burden provide some buffer, helping the country absorb external shocks.

In its latest Regional Economic Prospects report in February, the bank forecasted that the Turkish economy would expand by 4% by the end of 2026, following 3.7% in 2025.

Looking across the region, the report said the conflict pushed up energy prices due to disruptions in production and transport routes in the Persian Gulf.

The EBRD estimated that if oil prices remained above $100 per barrel and supply chain disruptions persisted, global growth could fall by at least 0.4 percentage points, while inflation could rise by more than 1.5 percentage points. Gas markets also remained tight, with European storage levels below recent years, suggesting prices could stay elevated even if tensions eased.

Beyond energy, the report said spillovers were spreading into trade, tourism, and remittance flows. Disruptions in Gulf trade routes risked affecting key industrial inputs such as aluminium, petrochemicals, and plastics, adding to global cost pressures. At the same time, tourism-dependent economies in the region were likely to see weaker visitor demand.

Remittances from Gulf countries—an important income source for economies such as Egypt, Jordan, and Lebanon—also came under pressure as economic activity slowed.

According to the bank’s calculations, Lebanon ranked as the most affected country, driven by its reliance on remittances from Gulf countries, high external debt, and strong trade links. Jordan and Iraq followed, reflecting their dependence on trade routes, energy flows, and remittance income.

Egypt also ranked among the more exposed economies, facing higher borrowing costs, reliance on external financing, and sensitivity to tourism and remittances.

The EBRD added that the economic effects of the conflict could persist beyond the end of hostilities, particularly if elevated energy prices and disrupted trade flows continued to weigh on growth.

1 min read

1 min read

1 min read

1 min read