Newsletters

Newsletters

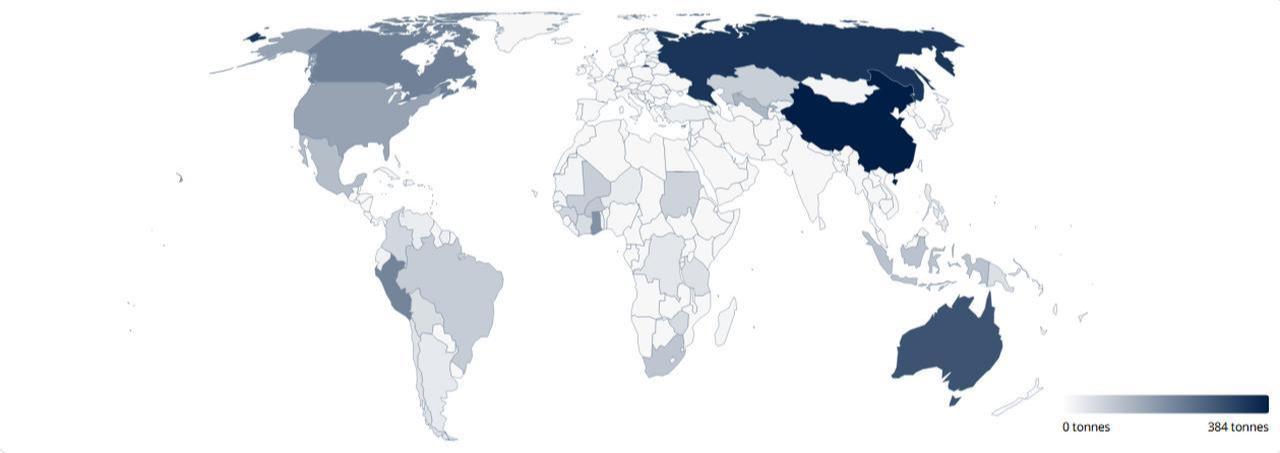

Türkiye remained among the world's top 30 gold-producing countries in 2025 despite a second consecutive annual decline in mine output, according to World Gold Council (WGC) data.

Gold production totaled 28.1 metric tons last year, down from 32 tons in 2024 and 36.8 tons in 2023, extending the country's downward production trend for a second consecutive year.

Global gold mine production increased 2% year-over-year to 3,816.8 metric tons in 2025, up from 3,740.6 tons in 2024.

China remained the world's largest producer after increasing output 1.1% to 384.3 tons. Russia followed with 345 tons, up 4.5% from a year earlier, while Australia expanded production 3.2% to 293.2 tons.

Canada posted one of the stronger gains among the leading producers, with output rising 5.2% to 213.3 tons, while Peru's production climbed 2.8% to 208.9 tons.

Among the other major producers, Ghana recorded the largest increase in the top 10, with production surging 21% to 187.3 tons. In contrast, output declined in the United States, falling 3.7% to 157 tons, while Uzbekistan's production slipped 2.9% to 125.4 tons and Mexico's dropped 3.4% to 113.5 tons.

The gains recorded by several of the world's largest producers more than offset declines elsewhere, lifting global mine output to its highest level on record.

Driven by record-breaking gold prices, consumer demand in Türkiye weakened in 2025 as higher costs discouraged purchases, although investment interest remained supported by safe-haven demand.

Demand for gold bars and coins totaled 71.1 metric tons, down 37% from 112.2 tons a year earlier, while jewellery demand fell 20% to 32.8 tons, its lowest level since 2020. Combined consumer demand declined to 103.9 tons from 153.1 tons in 2024.

The trend was part of a broader global shift. Worldwide gold demand, including over-the-counter trading, surpassed 5,000 metric tons for the first time in 2025, while its value jumped 45% year-over-year to a record $555 billion.

The market has continued to evolve in 2026. In the first quarter, Turkish demand for gold bars and coins rose 29% year-over-year to 26.1 metric tons, with purchases reaching a record $4 billion in value. Jewelry demand, meanwhile, fell 23% to 6.8 tons.

The World Gold Council expects geopolitical tensions, continued central bank buying, and resilient demand for gold-backed ETFs, bars, and coins to support the market throughout 2026, while jewelry demand is likely to remain under pressure in a high-price environment.

1 min read

1 min read

1 min read

1 min read