Newsletters

Newsletters

On July 14, President Trump hosted Iraqi Prime Minister Ali al-Zaidi at the White House and stated that “massive” oil deals would be announced in the coming weeks.

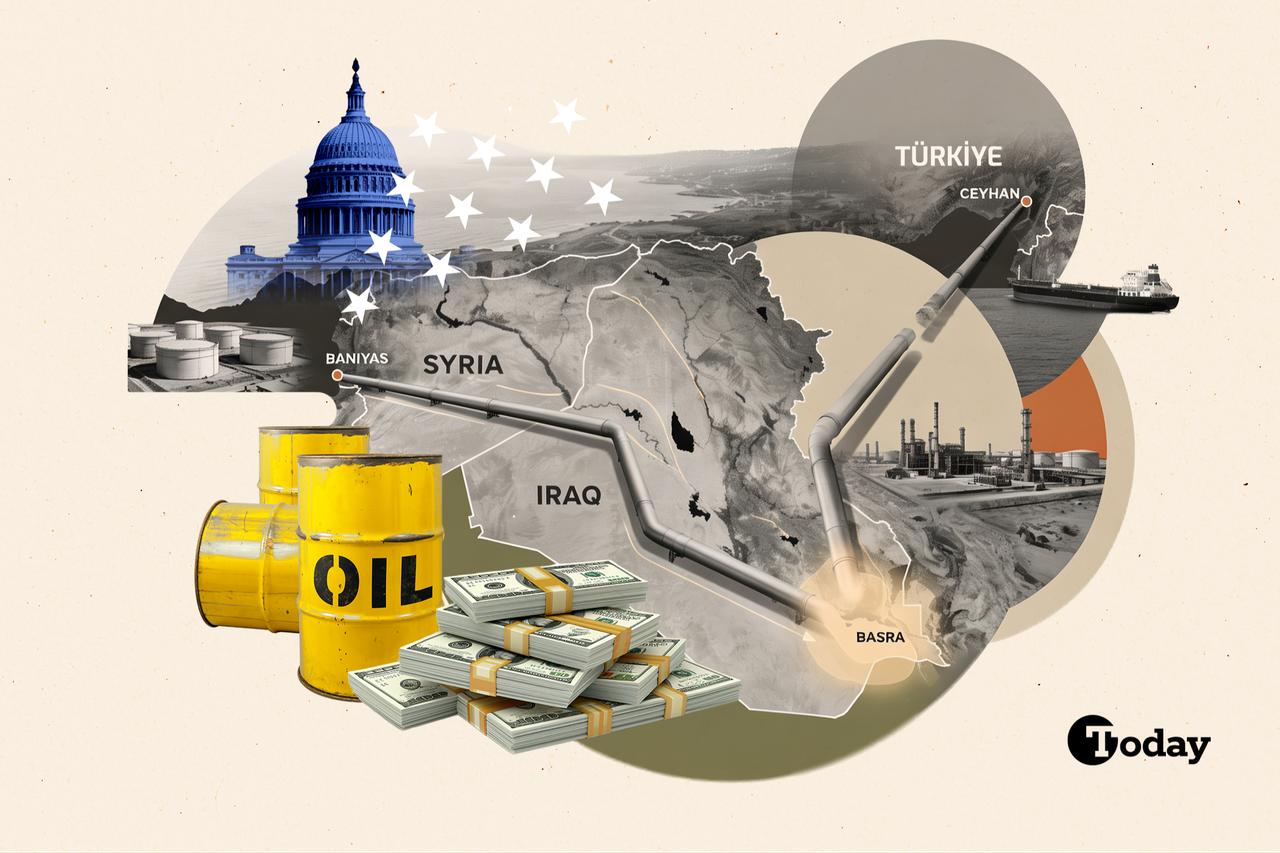

Around the same time, the U.S. State Department confirmed its official support for pipeline projects designed to transport Iraqi oil to Syria’s port of Baniyas and said it expects American companies to play a role in their construction.

Washington’s Special Envoy for Syria and Iraq Tom Barrack has been working on this file for months, while Chevron, TotalEnergies, TI Capital, and Qatar’s UCC Holding are all involved in the discussions. In other words, Washington’s backing is no longer a matter of speculation or behind-the-scenes reporting; it is now declared policy.

The United States aims to develop the Basra-Haditha backbone and the Baniyas outlet as an alternative energy corridor to the Strait of Hormuz.

At first glance, this development may appear positive from Türkiye's perspective. Reducing Iraq’s dependence on Hormuz, enhancing regional energy security, and creating new outlets to the Mediterranean seem broadly aligned with Ankara’s interests.

Yet in energy geopolitics, the key question is always a different one: access to the Mediterranean is one thing, but through which country?

The answer to that question will directly shape Türkiye's strategic weight in the Eastern Mediterranean. After all, being an alternative export route is not the same thing as being an energy hub, and the center of gravity of the routes currently on the table does not run through Türkiye.

Iraq possesses one of the world’s most fragile oil export systems. Before the war, the country was producing more than 4.1 million barrels per day and exporting roughly 3.4 million barrels through the Basra terminals.

Approximately 95% of its exports depended on a single chokepoint: the Strait of Hormuz. More than 90% of government revenue was also tied to oil.

After Feb. 28, the effective closure of Hormuz exposed the full cost of that vulnerability. As storage facilities filled up, wells had to be shut in. By April, production had fallen to around 1.4 million barrels per day—the lowest level recorded since the 2003 invasion.

According to energy analytics firm Vortexa, Iraq’s seaborne exports in May amounted to just 8% of the previous year’s average, representing a collapse to roughly 250,000–300,000 barrels per day. For Iraq, this translated into tens of billions of dollars in lost income.

Perhaps the clearest illustration of Baghdad’s predicament was the sight of tanker trucks crossing into Syria through the al-Tanf/al-Walid border crossing: as many as 500 trucks per day, carrying no more than 100,000–125,000 barrels in total.

An export machine designed to move millions of barrels per day was reduced to tanker convoys. Moreover, the damage may not be temporary. Extended well shut-ins create risks of reservoir pressure loss and corrosion, meaning that part of Iraq’s production capacity may not return to previous levels even after the crisis ends.

Against this backdrop, it is entirely rational for both Iraq and the United States—one of the principal actors in the crisis—to seek alternative export routes. And that is precisely where the problem begins.

What is commonly discussed in public under the label of the “Haditha-Baniyas project” consists of two distinct projects, and distinguishing between them is critical for any serious analysis.

The first is the Basra-Haditha pipeline: a new domestic backbone that would connect Iraq’s southern production centers to the Haditha junction in the country’s west, entirely within Iraqi territory.

The project approved by Baghdad carries an estimated cost of $4.6 billion and a planned capacity of 2.25 million barrels per day. Approximately $1.5 billion has been allocated for 2026, with completion targeted for 2028.

This pipeline is not an export route. Rather, it would transform Haditha into a distribution hub from which southern Iraqi crude could be directed toward Syria, Jordan, or Türkiye.

The second is the Baniyas branch: the export connection extending from Haditha through Syria to the Mediterranean. Two options are currently under discussion.

The first involves rebuilding the historic Kirkuk-Baniyas pipeline, an approximately 850-kilometer (528-mile) route that has remained out of service since 2003. Syrian officials acknowledge that most of the pumping stations along the route have been destroyed. This is not a matter of simple repairs but of reconstruction from the ground up, with cost estimates reaching as high as $8 billion.

Under revival scenarios, the initial phase would operate at a relatively modest capacity of around 300,000 barrels per day. The second option is an entirely new pipeline from Haditha to Baniyas.

An international consulting firm has been tasked with the feasibility study, while Basra Oil Company has signed an advisory agreement with the Houston-based engineering firm KBR. The capacity figures being discussed for this route range between 700,000 and 1.5 million barrels per day.

In other words, the claim that “2.5 million barrels per day will flow directly to Baniyas” is incorrect; that volume refers to the internal Basra-Haditha backbone. Yet this correction does not diminish the strategic challenge—it clarifies it.

Even the upper-end scenario of 1.5 million barrels per day for the Baniyas branch would be six to seven times larger than the current actual flow through the Kirkuk-Ceyhan pipeline, and that oil would reach the Mediterranean without passing through Türkiye.

This is not merely a question of transit revenues. Energy corridors are also corridors of political influence. The flow of 1–2 million barrels of oil per day through a country’s territory generates far more than economic income; it brings diplomatic weight, bargaining power during crises, attractiveness for infrastructure investment, and broader regional influence.

From the perspective of Ahmad al-Sharaa’s government, an Iraqi oil pipeline reaching Baniyas is therefore entirely rational.

According to various analyses, the pipeline could generate approximately $150 million to $200 million in annual transit revenue for Syria—a meaningful sum for an economy emerging from years of war, particularly given its potential to stimulate investment in ports and refining infrastructure.

Baniyas, home to the country’s largest refinery with a capacity of roughly 140,000 barrels per day, is naturally positioned as the leading candidate to receive Iraqi crude.

The removal of Syria from the list of state sponsors of terrorism has also opened the door for American companies. French President Emmanuel Macron becoming the first European leader to visit Damascus after the fall of Assad, together with TotalEnergies CEO Patrick Pouyanne’s remark in Damascus that “if you want to transport Iraqi oil without relying on Hormuz, Syria becomes a key transit country,” are both indicators of the emerging landscape.

At this stage, the assumption that every development benefiting Syria will automatically benefit Türkiye should be re-examined. A project that serves Damascus’ interests does not necessarily serve Ankara’s interests as well. In some cases, the interests of the two countries may directly compete.

The Haditha-Baniyas project is a prime example. Rather than complementing Türkiye’s vision of becoming an energy hub, it would establish a parallel energy center on the Eastern Mediterranean coast.

The most likely route passes through Anbar and eastern Syria, where Daesh cells remain active. Iranian-backed militias that openly oppose energy cooperation with Damascus could target the pipeline.

The Kurdistan Regional Government (KRG) also views the Haditha-Baniyas project as a development that weakens its bargaining power vis-a-vis Baghdad and may generate domestic political resistance.

The war has also demonstrated that even supposedly secure bypass infrastructure such as Petroline and Fujairah is not immune to attack. Both were targeted by Iranian drones, underscoring that overland energy corridors are not invulnerable.

On the financing side, investors continue to demand proof that the government in Damascus can maintain long-term control over the territory through which the pipeline would pass.

All these points are valid. None of them, however, should offer much comfort to Türkiye. The strategic challenge lies not in the project’s timeline, but in its direction.

Washington’s declared political commitment, the involvement of major international energy companies, and the fact that the internal backbone has already been approved and financed all indicate that the western corridor has evolved beyond a concept on paper into a project backed by diplomacy, capital, and institutional support.

Even a delayed, gradual, and relatively low-capacity Baniyas route would break Ceyhan’s de facto monopoly over Iraqi oil exports and structurally erode Ankara’s bargaining power.

1 min read

1 min read

Ankara needs to move beyond the mindset of, “Iraqi oil is reaching the Mediterranean through friendly Syria, how wonderful.” In energy geopolitics, what matters is not simply that oil reaches the Mediterranean, but through which country it travels.

Türkiye’s priority should be to restore the Kirkuk-Ceyhan pipeline to high utilization rates and to ensure that as much of the Basra-Haditha corridor as possible is directed toward Ceyhan.

Haditha is a junction; which port ultimately receives the oil will be determined by cost, security, and political choice.

At the same time, the Development Road project and energy corridors should be considered together. Türkiye should offer Iraq not merely a pipeline, but a comprehensive logistics and energy network.

A more realistic approach toward Syria is also required. The interests of Damascus and Ankara will not always align. For that reason, Türkiye should focus not on ignoring the Baniyas option, but on managing its implications.

If tomorrow’s energy map directs large volumes of Iraqi oil toward Syria’s Mediterranean coast, the loser will not be only the Kirkuk-Ceyhan pipeline. It will be the strategic energy hub position that Türkiye has spent the last two decades trying to build in the Eastern Mediterranean.

1 min read

1 min read