Newsletters

Newsletters

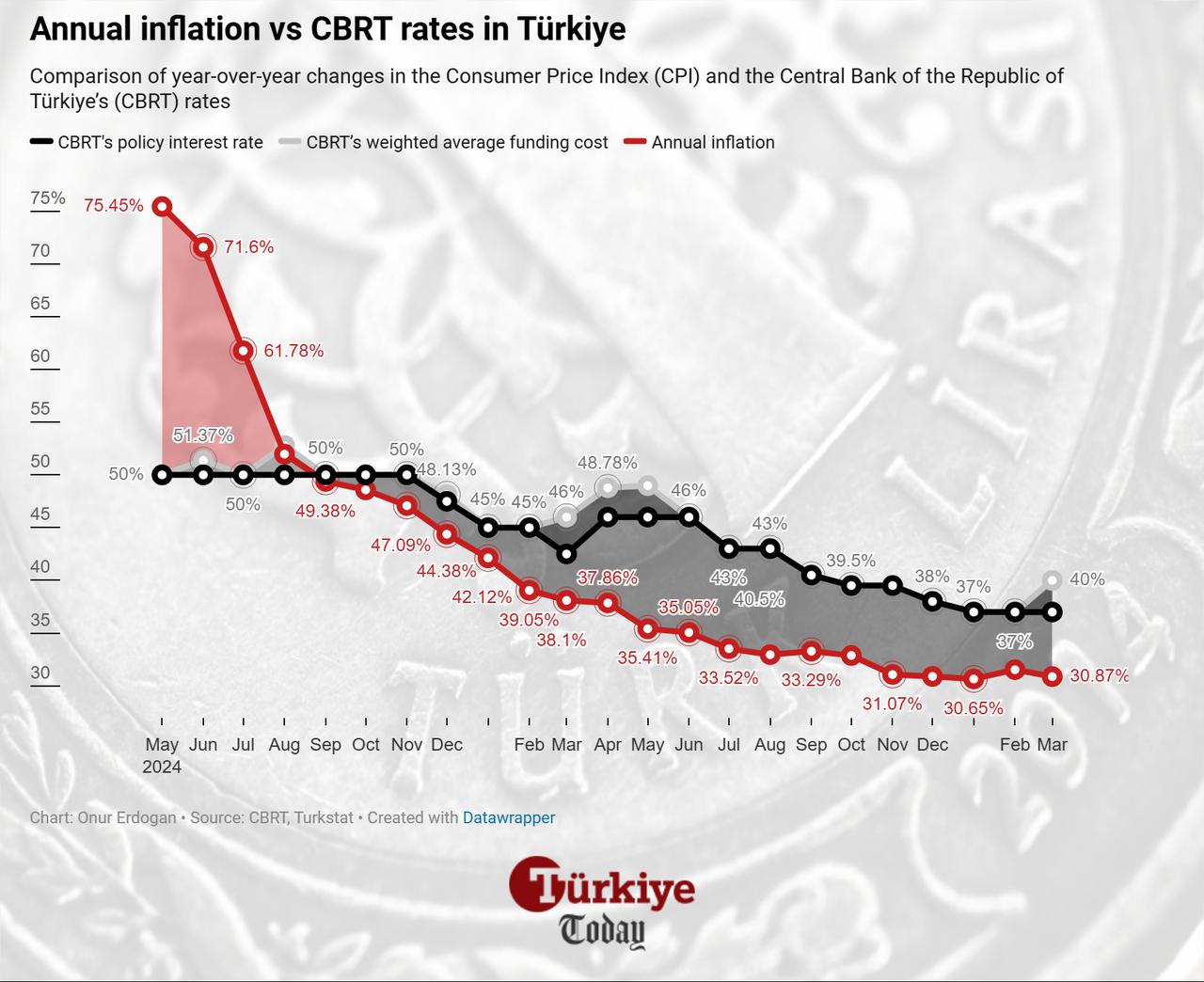

The Central Bank of the Republic of Türkiye signaled it is not in a rush to act, holding its policy rate at 37% while leaving the door open to rate cuts as early as July, according to analysts.

The decision was in line with market expectations, though some had anticipated a 300-basis-point hike to lift the policy rate to the current funding cost of 40%.

Instead, the bank struck a more balanced tone and is likely to continue funding at the higher 40% overnight rate, supported by improved conditions following a ceasefire between the U.S. and Iran to negotiate a potential deal to end the conflict.

In its assessment, ING pointed to a rebound in reserves alongside growing signs that economic activity is losing pace as key factors behind the decision.

Since early April, the central bank has rebuilt around $20 billion in reserves, partly supported by a reversal in capital outflow pressure as geopolitical tensions eased, it noted. That recovery has helped offset a portion of the $50 billion in foreign exchange sales recorded in March.

At the same time, recent indicators suggest softer domestic demand, a shift the central bank has openly acknowledged, the report added.

Analysts say the latest move indicates policymakers do not see a need for additional tightening at this stage, instead leaning toward a gradual normalization path.

"In the near term, the CBRT will remain in a wait-and-see mode," ING noted, adding that officials are likely to hold off before deciding whether to bring the effective funding cost closer to the policy rate.

According to BBVA Research, the decision reflects a cautious but slightly growth-oriented stance, even as inflation expectations worsen.

Analysts point to improving reserves, a decline in risk premiums, and relatively low dollarization as factors supporting the decision to hold. At the same time, authorities appear to view geopolitical risks as temporary.

Still, inflation remains a concern. April data is expected to show further deterioration, as the central bank indicated in its statement, with annual inflation seen hovering around 32% through July.

The current account deficit, which reached $35 billion annually in February, also continues to weigh on the outlook, suggesting pressure on reserves and the exchange rate may persist, BBVA noted.

Looking ahead, analysts expect funding costs to start easing from June, gradually moving closer to the policy rate. If that process unfolds smoothly, limited rate cuts could come onto the table from July.

Based on current forward energy prices, year-end inflation is projected at around 28.5%, while the policy rate is seen declining to a maximum of 35% by that time, it added.

1 min read

1 min read

1 min read

1 min read