Newsletters

Newsletters

This article was originally written for Türkiye Today’s weekly economy newsletter, Turkish Economy in Brief, in its June 15 issue. Please make sure you are subscribed to the newsletter by clicking here.

When hopes are rising in the Middle East, oil prices have fallen below $90 for the first time in two months, and the Central Bank of the Republic of Türkiye (CBRT) has kept interest rates unchanged. Attention has once again turned to the Turkish economy.

Looking briefly at two key developments:

Just one day after the CBRT opted to remain in a “wait-and-see” position, positive developments emerged on the geopolitical front. If the agreement materializes and the Strait of Hormuz reopens, oil prices could decline further.

It is worth recalling that oil was trading at $61 at the beginning of the year and around $73 when the conflict began.

A decline in oil prices is critical for four major balances in Türkiye: inflation, interest rates, the current account balance, and exchange rates. Cheaper oil means lower foreign currency demand and a smaller current account deficit. It also helps ease inflationary pressures and creates room for lower interest rates.

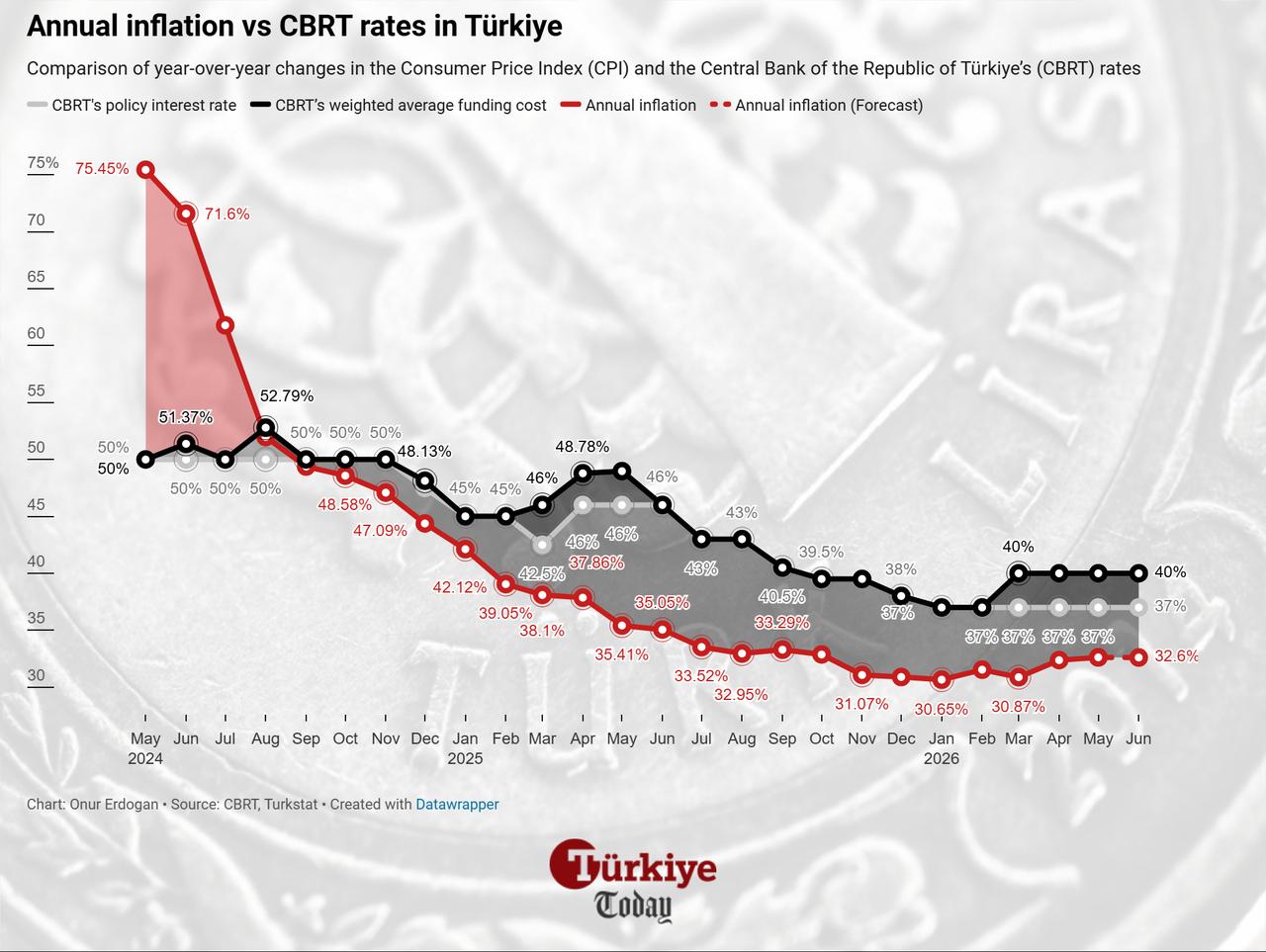

Inflation, which has faced a significant test since the conflict began in early March, peaked at 4.2% month-on-month in April before easing to 1.7% in May.

Annual CPI inflation, which stood at 30.9% in March, rose to 32.6% last month. At this stage, inflation in Türkiye has shown signs of “stickiness,” remaining within the 30.50%-33.50% range for 11 months since July 2025.

Türkiye’s current account recorded a deficit of $5.7 billion in April, bringing the 12-month deficit to $37 billion.

Excluding higher oil prices and on an energy- and gold-adjusted basis, the current account posted a surplus of $319 million in April.

The recent decline in gold imports has partially offset the cost of oil-driven energy imports.

During this period, the CBRT’s tight monetary policy and active management of foreign exchange markets helped maintain stability in the Turkish lira. Reserves were occasionally used to support this effort.

The USD/TRY exchange rate, which stood at 44.42 at the beginning of March, ended last week at 46.25.

At this point, Türkiye’s path back to lower inflation and the potential start of a rate-cutting cycle remain closely linked to developments in the Middle East.

In an analysis by Yapi Kredi, the bank noted that energy costs could decline if an agreement is reached in the Middle East, adding that “under such a scenario, an easing cycle at the CBRT could come onto the agenda.”

A report by Kuveyt Turk Yatirim highlighted that the CBRT has suspended one-week repo auctions since March 1 and has mainly provided funding through overnight lending rates. “Provided the improvement in inflation expectations continues, we believe the rate-cutting cycle could begin with a 100-basis-point reduction at the September 10 meeting,” the report stated, while forecasting a year-end policy rate of 34%.

International analysts have also offered notable comments. Luis Costa, Head of Emerging Markets Strategy at Citigroup, said that positive developments in the Middle East would significantly ease risk perceptions toward Türkiye.

He added that tourism-related foreign currency inflows are expected to increase during the summer and that the CBRT may remain in a holding pattern.

Economist Banu Kivci Tokali likewise stated that the CBRT continues to maintain its “wait-and-see” stance and that, barring major shocks, interest rate hikes are not on the agenda, while rate cuts could begin as early as September.

Markets have already begun pricing in the positive scenario, with equities leading the response. The BIST 100 index tested the 14,000 level on Friday and ended the week at 13,938, up 1.8%.

A period in which expectations for the Turkish economy become more positive may now be approaching.

Under an optimistic scenario, stronger tourism-related foreign currency inflows during the summer, easing inflation in key components such as food and energy, an improvement in the current account balance, and reduced pressure on exchange rates could pave the way for a return to policy-rate normalization in July or August, followed by interest rate cuts.

Let us conclude with remarks made last week by Turkish Treasury and Finance Minister Mehmet Simsek at the General Assembly of the Turkish Banks Association:

“Shocks may occasionally cause delays. These shocks are beyond our control, but they are not an excuse. What matters is progress. The disinflation process will continue after a delay of a few months and will get back on track.”

6 min read

6 min read