Newsletters

Newsletters

Treasury and Finance Minister Mehmet Simsek has been getting a lot of flak—again—from the Turkish media, with a common theme being the supposed failure of his economic program.

Turkish daily Yeni Safak seems to have a particular problem with him. They ran a similar campaign against former Central Bank of the Republic of Türkiye (CBRT) governor, Naci Agbal, whose firing turned out to be an absolute disaster.

Minister Simsek would likely be the first to admit he is not above criticism. He would also agree that the road, since his appointment in the Spring of 2023, has been marked by its share of mistakes.

I, for one, argued for more aggressive frontloading of the policy tightening that was needed to rein in inflation at the outset of the current program. However, the desire to head off a sharp growth slowdown led to a looser policy stance than was perhaps advisable. The result is inflation that remains higher and stickier than initially projected.

That was a political trade-off. These things happen in political economy.

It is also true that Simsek has faced a series of formidable obstacles beyond his control. The aggressive foreign exchange adjustment in mid-2023 was virtually forced by devaluation expectations that had already solidified before the elections. Subsequent political shocks, such as the arrest of former Istanbul Mayor Ekrem Imamoglu, further complicated the landscape.

Beyond politics, unfavorable agroclimatic factors weighed on the program, while deep-seated structural issues in the service sector, education, and housing markets continued to hinder progress. Now, the onset of Gulf war III presents yet another significant external headwind.

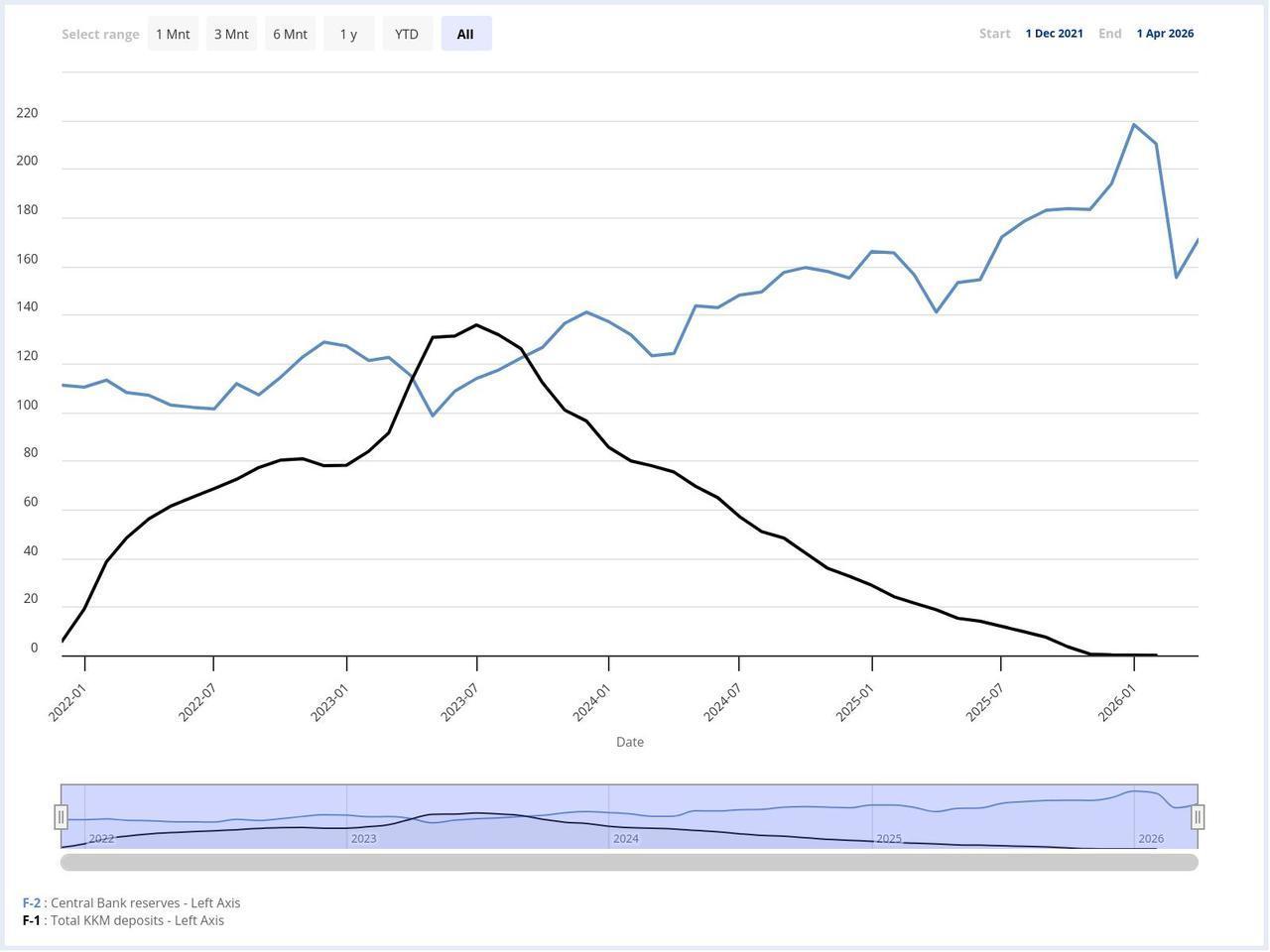

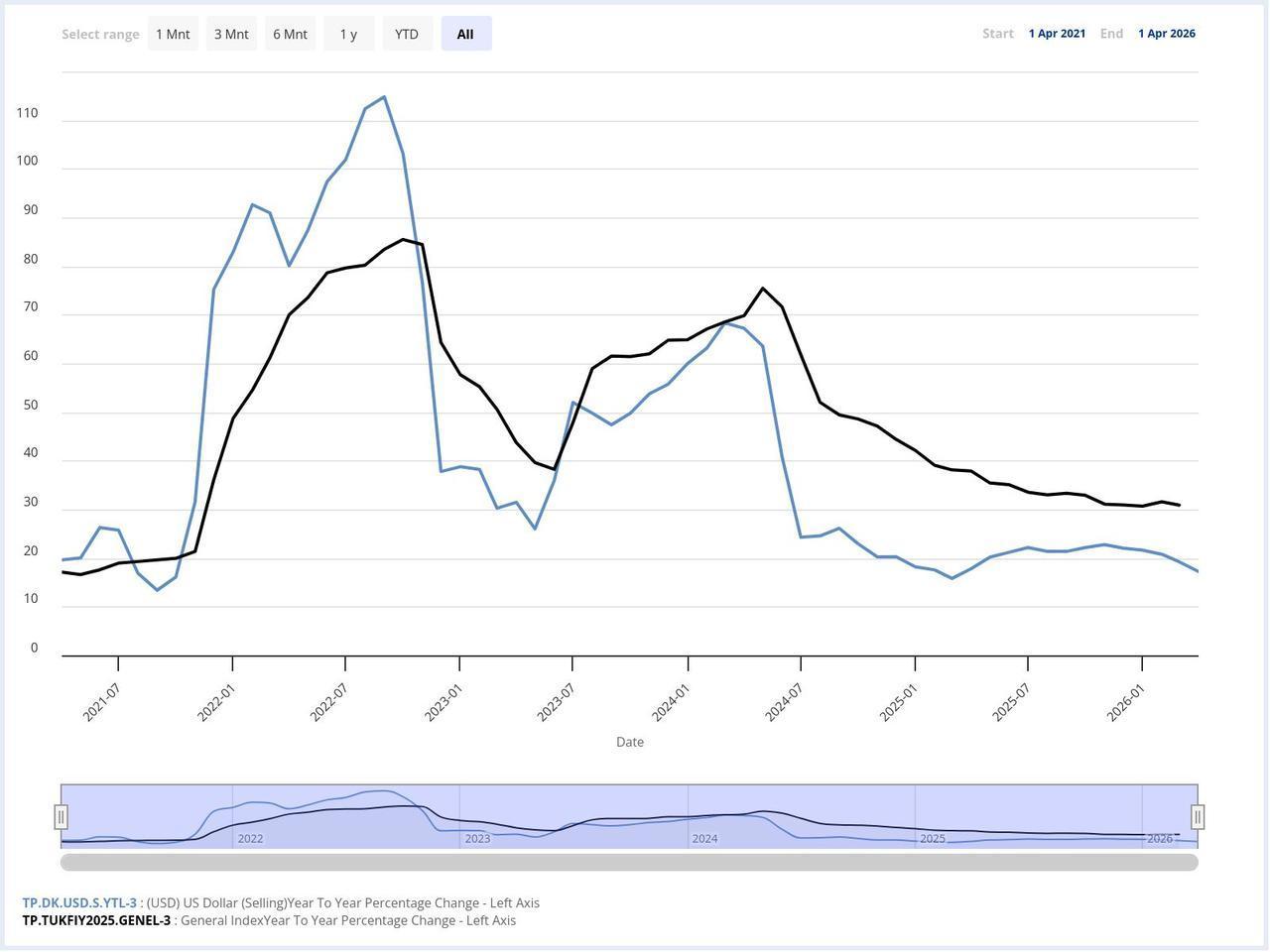

And yet, despite these challenges, significant progress has been made. Inflation was brought down from over 70% to just over 30%. The potentially disastrous FX-protected deposit scheme (KKM) was dismantled, falling from over $140 billion to next to nothing. This was achieved while nearly doubling reserves to over $200 billion and providing full coverage of external financing needs—a milestone reached for the first time in recent memory.

The lira has now stabilized and is on a gradually depreciating but predictable path. Dollarization has stalled, and international borrowing costs have been slashed, with ratings set on a positive path again. The fiscal deficit was reined in, within reach of just 3% of gross domestic product (GDP) this year, and public debt was held below 30% of GDP.

Türkiye rode through the shock of the Imamoglu case and of the recent U.S. attack on Iran with some reserve depletion but with relatively well-behaved markets. Systemic risks—which were front and center in early 2023—were avoided.

Given the marked fiscal improvement under Simsek, it appears current popularity issues are largely shaped by the success of his crackdown on the informal economy and improved tax compliance. No one likes paying tax, but the deployment of technology—and a notably more invasive policing by tax authorities—has placed fiscal accounts on a much stronger footing.

Ultimately, Simsek should be commended for delivering results where many predecessors failed, particularly when such gains were easy to promise but historically difficult to achieve.

These represent significant achievements for Team Simsek. If you had suggested in early 2023 that such results would be delivered within three years, many would have laughed and not believed you.

In addressing the CBRT’s response to the latest travails in the Gulf, economist Robin Brooks has argued that given Türkiye’s elevated and widening current account deficit, the lira should have been allowed to devalue—much as the Central Bank of Egypt permitted—rather than depleting scarce FX reserves in its defense.

While the CBRT should ideally operate independently of the Finance Ministry, the economic reality remains that a finance minister must have a say in the FX regime being pursued, particularly during pivotal moments.

But Türkiye successfully navigated the early weeks of the war. While some reserves were depleted, the FX regime remained intact, and roughly two-thirds of those reserves have since been rebuilt as peace prospects improve. The CBRT allowed an orderly exit for foreign investors, who in turn demonstrated confidence by returning at the first opportunity.

In response to the Brooks critique, it is necessary to be mindful of Türkiye's specific vulnerability to oil price shocks; all else being equal, every $10 increase in the price of a barrel adds $4 billion-$5 billion to the current account deficit and approximately 1% to inflation.

Given high levels of dollarization, allowing the lira to depreciate would have accelerated inflation pass-through and risked a vicious downward spiral. While such a spiral remains a threat should oil prices stay elevated, the CBRT’s decision to view the price shock as temporary was a logical one, an opinion I share with Brooks. With inflation already at high levels, the priority was to avoid further de-anchoring inflationary expectations.

Brooks would have advised letting the currency adjust and subsequently hiking policy rates to counter the resulting inflation pass-through. It is a fair point, but it raises a fundamental question: if a shock is deemed temporary, is that not precisely what FX reserves are for—to provide insulation against unforeseen events?

Furthermore, the CBRT has made it abundantly clear that should the war in the Gulf linger, a recalibration would follow. I take this to imply that the currency would then be allowed to adjust to the new reality of sustained higher energy prices, with policy rates following suit.

Predictably, exporters have voiced frustration that the exchange rate has served as the primary anchor for disinflation, leading to a significant real appreciation. With inflation remaining stubbornly high, this appreciation has been severe, creating a widespread perception—among citizens and tourists alike—that Türkiye has become prohibitively expensive. This is why I argued for a tighter policy stance at the outset; while such a move would have required a larger sacrifice in terms of growth, it likely would have delivered lower inflation more rapidly, resulting in a slower appreciation today.

But as they say, we are where we are, and Simsek adopted the more moderate path of disinflation as a reflection of the political realities he was facing. Indeed, even the large initial policy rate hikes from the CBRT, from 8.5% to 50%, were greeted with much opposition and criticism.

And now, I would argue, what is the alternative?

It appears that those lobbying for Simsek’s head now want policy loosening to achieve a faster pace of policy rate cuts, followed by a weaker lira to address competitiveness concerns.

This seems like madness. Faster tracking policy rate cuts—already too rapid in my view—against a backdrop of the risks around the Gulf war, and presumably on the back of Simsek getting fired, would be absolute suicide. Such a shift would likely trigger a sharp and sustained depreciation of the lira, sparking an immediate spike in inflation and creating even deeper long-term challenges for national competitiveness.

And if you are going to replace Simsek, I would ask, with whom? Would any successor truly command more credibility? The answer is almost certainly no. Such a move would effectively set Türkiye back three years, leaving the country once again fretting over the same systemic risks facing the country.

Clearly, Türkiye faces a competitiveness challenge, but the most effective solution lies in structural reforms rather than policy loosening and devaluation. It is evident that Simsek recognizes this reality, having recently advocated for using the urgency created by the Gulf crisis as a catalyst to fast-track these reforms.

Similarly, measures should be taken to increase energy-sector efficiency to reduce dependency on imports and cut energy use more broadly. Many of these steps are already in place but there is a need to accelerate them. Efforts to formalize the economy, as reflected in the increased tax take, should be made.

These reforms should prioritize deeper integration with Europe, with defense technology serving as a strategic sweetener to secure an enhanced Customs Union. Education reform to upgrade the labor force's skill should be a priority, alongside agricultural restructuring to mitigate the recurring impact of agroclimatic conditions on food prices.

Similarly, measures should be taken to increase energy-sector efficiency to reduce dependency on imports and cut energy use more broadly. Many of these steps are already in place, but there is a need to accelerate them. Efforts to formalize the economy, as reflected in the increased tax take, should be made.

The opposition insists on steps such as a broader liberalization of society to improve checks and balances, the rule of law, and the need to fight corruption as part of improving the overall business and investment environment. All fair demands, but let's take into consideration U.S. Ambassador Tom Barrack’s comments this week about the advantages of a strongman rule, which understandably have gone down like a lead balloon with Türkiye's opposition.

It was also disappointing to hear European Commission President Ursula von der Leyen ranting about the importance of insulating Europe from being “influenced” by China, Russia and Türkiye. I really believe the World Trade Organisation (WTO) and Europe need Türkiye more now than ever as a strategic imperative, given the existential threat from Russia and with the United States' conduct with respect to Iran. Good luck to Europe holding its southern flank without the considerable capabilities of the Turkish military, its large and capable defense industrial complex, and drones.

Perhaps von der Leyen isn’t aware that Türkiye is still an EU candidate member state as well as a key NATO member, and will host the annual NATO summit this summer. Improved cooperation, integration, trade, and investment are now critical for Europe and Türkiye, given the threats, and our common interests.

The EU president evidently did not get the memo, if these comments are anything to go by. It is only by reinvigorating this relationship that both sides will benefit, providing Türkiye with critical momentum on its own reform path. A new and deeper Customs Union represents a vital first step—a clear quid pro quo that allows Türkiye to assist Europe in navigating its current defense challenges.

DISCLAIMER: The views and opinions expressed in this article are those of the author and may not necessarily reflect the editorial policy of Türkiye Today.

Timothy Ash is a regular contributor to Türkiye Today. In addition to his contributions, our outlet has been granted permission to republish his personal Substack articles.

1 min read

1 min read

1 min read

1 min read