Newsletters

Newsletters

This article was originally written for Türkiye Today’s weekly economy newsletter, Turkish Economy in Brief, in its May 11 issue. Please make sure you are subscribed to the newsletter by clicking here.

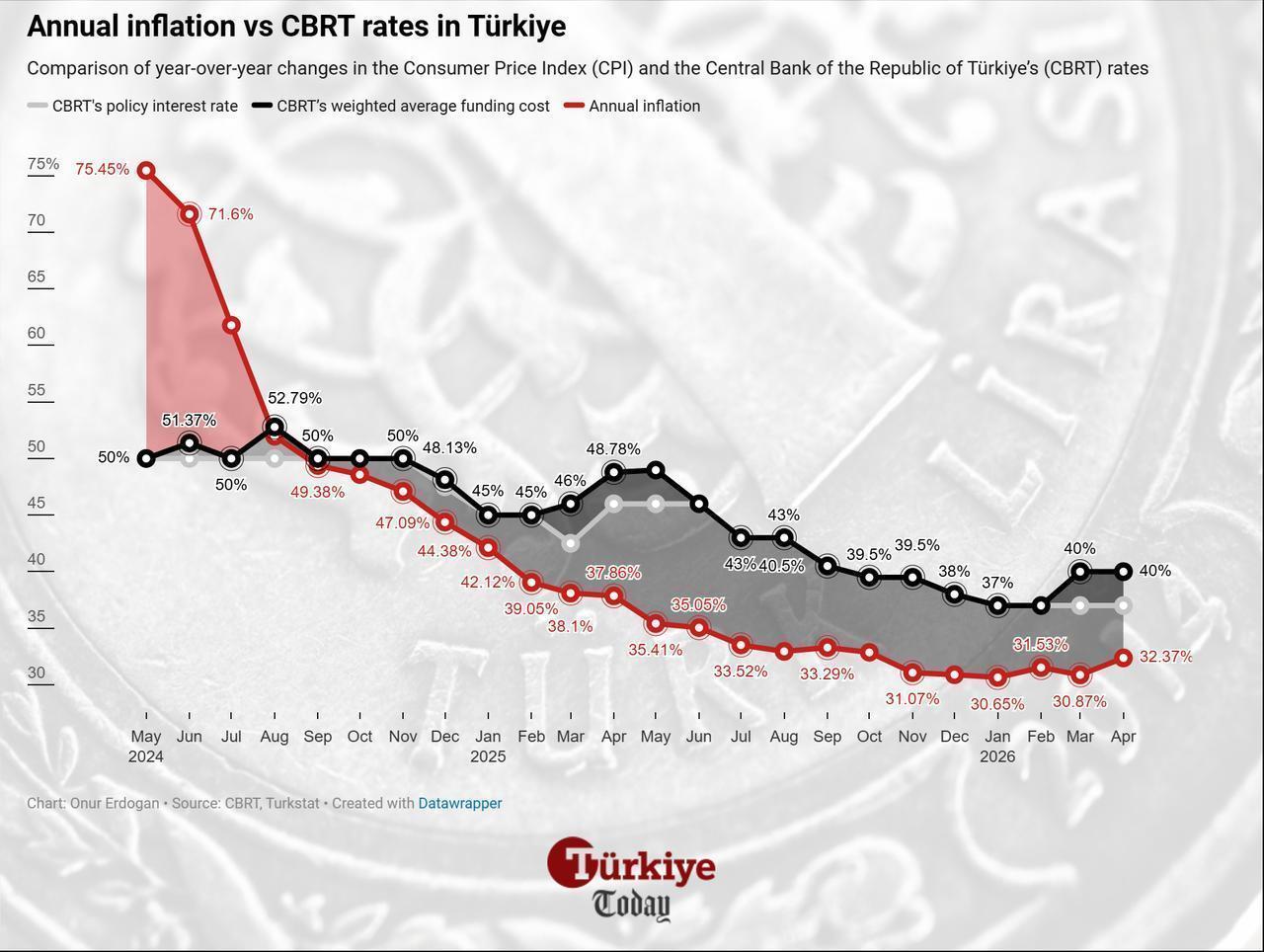

Two and a half months into the Middle East conflict, the economic toll of rising oil prices is becoming impossible to ignore. Türkiye’s monthly consumer inflation, which stood at 1.9% in March, jumped to 4.18% in April, painting a worse-than-expected picture. Annual inflation consequently rose from 30.87% to 32.37%.

The surge was felt across the board, with all 13 main categories recording increases. The sharpest rises were seen in the clothing and footwear (8.94%), housing (7.99%), and transportation (4.29%).

Consumer inflation in Türkiye was expected to rise by around 3.2% in April. Following the 4.18% reading, upward revisions in year-end inflation forecasts for 2026 also drew attention.

Local brokerage Is Investment has raised its year-end inflation forecast to 29%, up from the pre-war estimate of 24.5%. The report also outlined a likely path forward for monetary policy, noting that the central bank is expected to hold the interest rate through the summer months. A return to a rate-cutting cycle is anticipated starting in September, with the year-end policy rate forecast expected to land at 34%.

Akbank Economic Research projects year-end inflation at 30% under a base scenario where Brent crude oil remains at $95 per barrel and LNG prices at €50, while growth slows from 4% to 3% and the effects of the shock are absorbed through reserves and the public budget.

Despite optimism over a “continued ceasefire” and the possibility of a “lasting agreement,” oil prices closed above $100 last week. The continued closure of the Strait of Hormuz, through which nearly 20% of global oil supply passes, is preventing any meaningful decline in prices.

Alnus Investment also stated that the rapid rise in oil and related products following the closure of the Strait of Hormuz became more clearly visible in Türkiye’s April inflation data, while forecasting year-end CPI at 28.75%.

Regarding monetary policy, the report stated that the central bank will likely leave interest rates unchanged at its June 11 and July 23 meetings. The firm estimates that the policy rate could stand at 35% by the end of the year.

According to an analysis by Kuveyt Turk Investment, April inflation data highlighted a picture requiring caution. The brokerage identified adjustments in natural gas and electricity prices, along with increases in transportation services, were the main factors for the monthly spike. The food group made the largest contribution to monthly inflation with 0.95 percentage points.

In response to these pressures, the firm raised its 2026 year-end inflation forecast from 24.1% to 28.8%. Kuveyt Turk also expects the central bank to maintain its tight stance, leading to an upward revision of its year-end policy rate forecast from 32% to 34%.

Following the April inflation data, Central Bank of the Republic of Türkiye (CBRT) Governor Fatih Karahan delivered his first remarks at the Participation Finance Summit held in Istanbul: “We clearly saw the effects of the war in the April inflation data. We believe energy-driven impacts will continue in the short term.”

Karahan noted that while persistent energy pressures complicate the disinflation process, the bank's primary focus remains price stability. He emphasized that recent volatility will be carefully evaluated in upcoming monetary policy decisions.

Markets are now fully focused on the Second Inflation Report to be announced by the CBRT on May 14.

In its previous Inflation Report presentation on Feb. 12, the CBRT revised its 2026 year-end inflation forecast range from 13%-19% to 15%-21%, while maintaining its midpoint target of 16%.

Following the U.S.-Iran war and rising energy prices, the CBRT is expected to revise both its forecast range and its midpoint target upward, despite previously stating that the target would be maintained “unless extraordinary changes occur.” Tacirler Investment argues that “the upper end of the forecast range could approach 25%-26%.”

As a result, the scale of any possible revision to the midpoint target will also be important in terms of the message the CBRT sends regarding its disinflation path.

7 min read

7 min read