Newsletters

Newsletters

Rising oil prices in the wake of the Iran war are weighing on the Turkish economy but remain manageable, while the country’s economic program continues to move ahead as planned, Treasury and Finance Minister Mehmet Simsek told investors in London.

Simsek described the short-term impact of tensions in the Middle East as "negative, but manageable," indicating that the government is actively using fiscal space to absorb external shocks and limit spillovers into inflation.

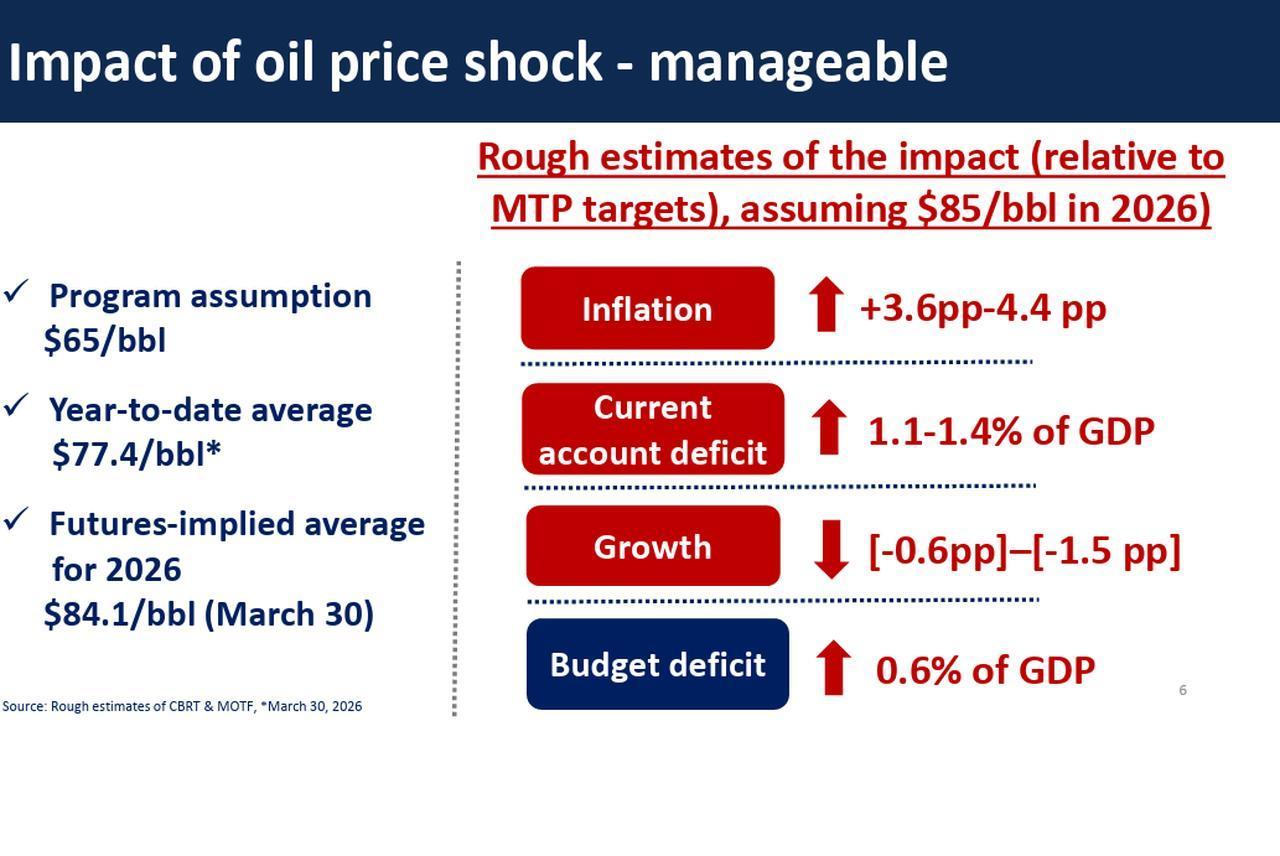

Officials estimate that if oil prices average around $85 per barrel in 2026, inflation would rise by 3.6 to 4.4 percentage points. The current account deficit is expected to widen to 1.1% to 1.4% of GDP, while growth is projected to slow by between 0.6 and 1.5 percentage points.

Türkiye’s annual inflation stood at 31.5% in February, while the current account deficit reached $32.9 billion in January. Economic growth was recorded at 3.6% in 2025.

The minister noted that a fuel tax buffer mechanism reintroduced at the start of the conflict is cushioning around 75% of fuel price increases, helping contain the direct pass-through to consumer prices and easing pressure on inflation.

Simsek pointed to early signs of easing inflation, noting that rent inflation has started to slow and that forward indicators suggest the decline will continue. Lower drought risk in 2026 is also expected to support food price disinflation.

He also highlighted a strong improvement in reserves, with gross reserves rising by $79 billion and net reserves excluding swaps increasing by $103.5 billion since May 2023. At the same time, external financing needs and debt ratios are trending lower, indicating a gradual strengthening in macroeconomic balances.

Simsek underlined that there is no change in the priorities of the current economic program, which remains broadly on track. The government continues to prioritize disinflation, fiscal discipline, and a sustainable current account balance, while pushing ahead with structural reforms to strengthen competitiveness and institutional capacity.

He also noted that the policy framework aims to rebuild buffers, reduce vulnerabilities, and maintain a rule-based economic approach while avoiding balance of payments pressures.

Simsek's presentation highlighted several drivers expected to support a more sustainable current account balance over time. These include increasing domestic oil and gas production, accelerating the green energy transition, reducing import dependency, and expanding the services surplus.

Services exports and tourism revenues continue to play a key role, while improvements in export composition and rising technological intensity are helping Türkiye move up the value chain.

Simsek also pointed to supply chain reconfiguration as a potential upside, suggesting that global trade shifts could channel more foreign direct investment into Türkiye, supported by its infrastructure, manufacturing base, and geographic position.

Simsek assessed the risk of spillover from regional conflict as extremely low, citing Türkiye’s deterrence capacity and NATO membership as key safeguards. He noted that the country’s exposure to Middle East trade and energy flows remains manageable, limiting the overall impact of regional instability.

Looking ahead, he suggested that the post-war environment could create new opportunities for Türkiye, including stronger positioning in trade corridors, increased reconstruction demand in neighboring regions, and a more prominent role as an energy and logistics hub.

1 min read

1 min read

1 min read

1 min read