Newsletters

Newsletters

This article was originally written for Türkiye Today’s weekly economy newsletter, Turkish Economy in Brief, in its June 8 issue. Please make sure you are subscribed to the newsletter by clicking here.

While global markets remain focused on the prospect of an agreement that could ease tensions in the Middle East, over three months have passed since the period of uncertainty began in March.

Although the ceasefire has largely held since early April, continued disruption in the Strait of Hormuz is helping keep oil prices elevated, while the latest exchange of strikes between Israel and Iran, which unfolded on Sunday, serves as a reminder that the risk of a broader regional escalation has not disappeared.

Brent crude rose to nearly $99 per barrel last week before closing at $92.8 and climbed toward $97.5 per barrel following the latest escalation.

Annual oil price forecasts are increasingly being revised upward toward the $75-80 range and above.

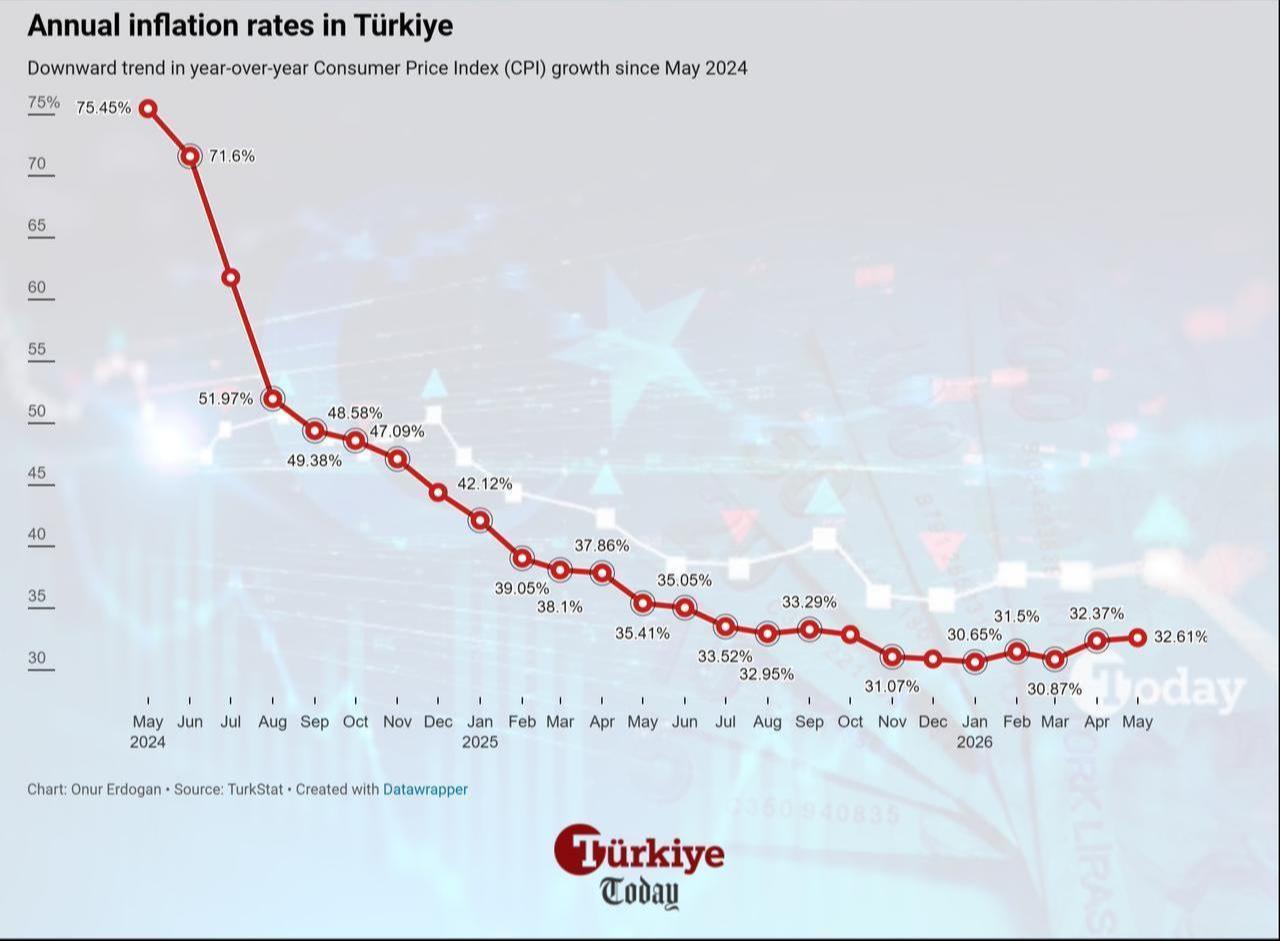

As high energy prices continue to fuel inflationary pressures, Türkiye released its third post-war consumer inflation report last week. Monthly inflation, which stood at 1.9% in March and 4.2% in April, slowed to 1.7% in May.

The figure marked a significant decline from April and came in broadly in line with market expectations. Annual inflation, however, increased from 30.9% in March to 32.6% in May.

A closer look at May inflation data shows notable price increases in several sectors outside of energy.

The Eid al-Adha holiday period and the start of the summer season appear to have boosted demand in clothing and footwear, transportation, particularly air travel, and restaurant and accommodation services.

Monthly price increases reached 11.3% in clothing and footwear, 2% in transportation, and 1.9% in restaurants and hotels.

On the other hand, food prices provided a positive contribution because of seasonal factors.

Prices in the food and non-alcoholic beverages category fell by 0.5% month-on-month, reducing headline inflation by 0.1 percentage point and offering some relief after a prolonged period of upward pressure.

Türkiye's economic performance in the first quarter was also announced last week.

The economy expanded by 2.5% year-on-year in the January-March period, falling short of the market expectation of 2.7%.

Following the inflation and growth data, attention has shifted to the Central Bank of the Republic of Türkiye (CBRT).

The Monetary Policy Committee is scheduled to meet on Thursday, June 11, when the bank will announce its latest interest rate decision.

CBRT Governor Fatih Karahan earlier said that the slowdown in demand observed during the first quarter had been confirmed, adding that April data also pointed to continued weakness.

Developments in the real economy, alongside inflation trends, are likely to influence the bank's decision.

Ahead of Thursday's meeting, the picture remains largely unchanged.

The CBRT kept its policy rate at 37% during its March and April meetings following the outbreak of conflict in the Middle East.

The bank has continued to provide market funding through the upper band of the interest rate corridor, which stands at 40%.

According to an assessment by Is Yatirim, the CBRT is expected to leave rates unchanged at its June 11 meeting.

“We believe economic policymakers want to keep the door open to implicit monetary easing, given the slowdown in growth and the possibility of the Strait of Hormuz reopening," the report said.

It added that the CBRT is expected to gradually bring funding rates closer to the policy rate in July and August, followed by 100-basis-point rate cuts at the September, October and December meetings, which would leave the year-end policy rate at 34%.

Kuveyt Turk Yatirim also expects the CBRT to keep its policy rate unchanged at 37%.

The firm said it believes repo auctions could resume in July and that a renewed rate-cutting cycle could return to the agenda at the Sept. 10 meeting. It forecasts a total of 300 basis points in rate cuts this year.

Akbank Economic Research similarly expects the CBRT to maintain its current stance, citing externally driven shocks, weak dollarization trends, signs of slowing economic activity, and recent macroprudential tightening measures.

The report added that, if conditions become favorable, the bank could return to one-week funding operations, effectively shifting market funding from 40% back toward the 37% policy rate.

Based on the latest economic data and forecasts from market professionals, the summer months are likely to be characterized by a wait-and-see approach to interest rates.

6 min read

6 min read