Newsletters

Newsletters

This article was originally written for Türkiye Today’s weekly economy newsletter, Turkish Economy in Brief, in its April 6 issue. Please make sure you are subscribed to the newsletter by clicking here.

The conflict in the Middle East has now entered its fifth week. While hawkish rhetoric stood out in U.S. President Donald Trump’s address to the nation last week, the April 6 date he had previously mentioned has also arrived.

All eyes remain on the conflict zone. The Strait of Hormuz is still closed. Commodity prices, especially oil, remain elevated, and uncertainty over when the war will end lingers on.

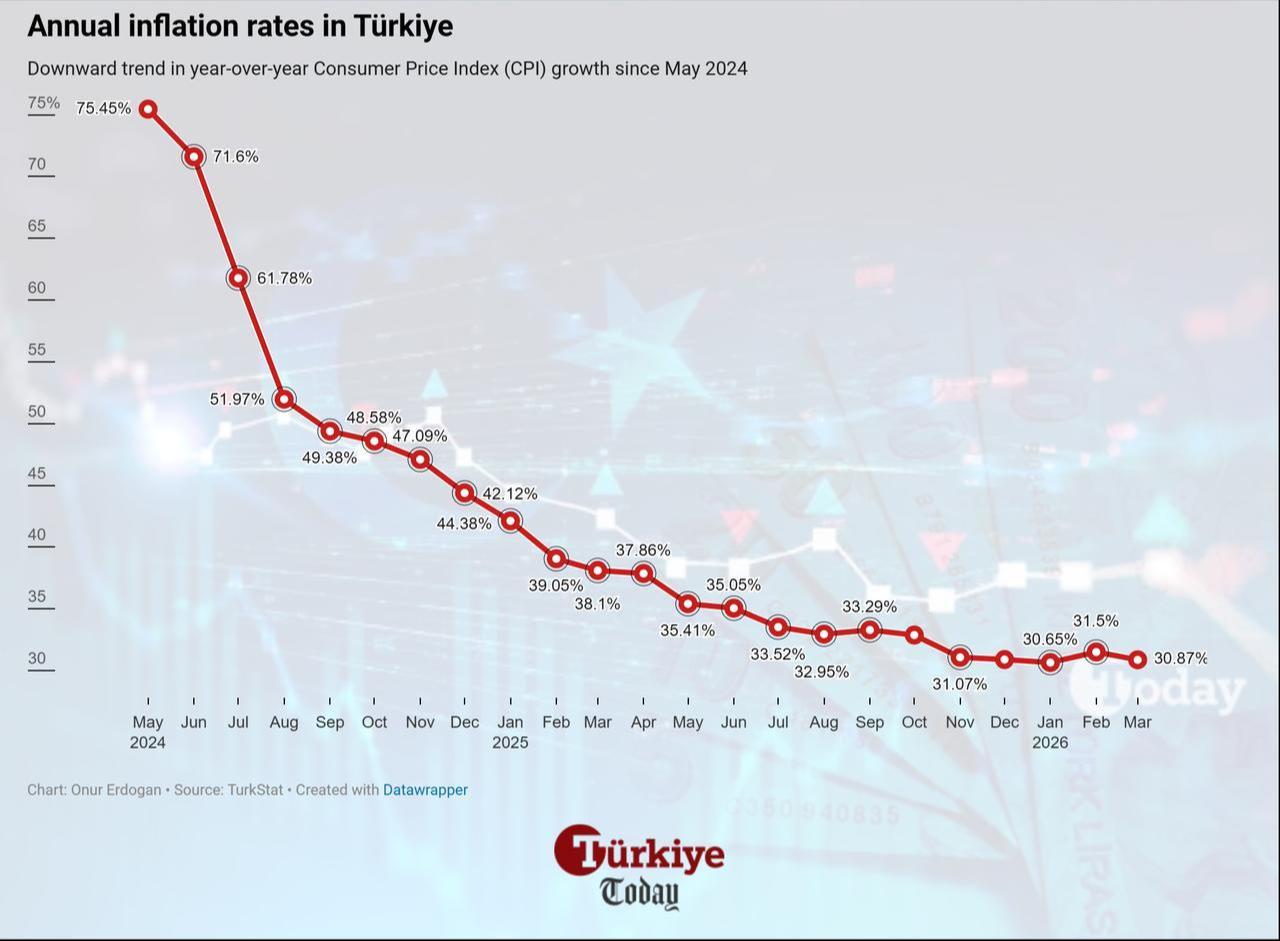

Turkish markets, meanwhile, saw the first impact of these developments in the March inflation data. Monthly inflation came in at 1.94%, below expectations of 2.40% in the AA Finans survey.

So why did inflation come in lower than expected? There are three main reasons:

As a result, a significant spike in inflation reflecting initial concerns was avoided.

External engagements by economic authorities also drew attention. Treasury and Finance Minister Mehmet Simsek and CBRT Governor Fatih Karahan met with investors and financial sector representatives in London on April 1-2.

The main topic of the two-day meetings was the impact of the Middle East conflict on Türkiye’s economy. Presentations emphasized that the effects of the war are “manageable.”

Karahan also told Anadolu Agency that using gold-based transactions during periods when foreign exchange liquidity needs support is a natural choice, noting that “a significant portion of these transactions are gold-FX swaps with set maturities, meaning the gold will return to our reserves when the term ends.”

Looking at the markets, the BIST 100 index closed last week at 12,936, up 1.88%, while the banking index rose 2.44%. The market appears to have shaken off some of the pessimism seen over the previous two weeks.

If there is light at the end of the tunnel and a window of opportunity, it may stem from ongoing ceasefire efforts in the Middle East, a decline in annual inflation from 31.53% to 30.87%, progress in disinflation, and reduced risk of a rate hike at the April 22 Monetary Policy Committee meeting.

If developments continue in this direction, it could confirm that markets have already seen the bottom during the recent shock.

As markets turn their attention to April’s rate decision, Kutay Gozgor, Research Director at Kuveyt Turk Investment, said March inflation delivered a positive surprise.

He noted that the main drivers of this easing were the sliding tax system, balancing energy prices and the rapid normalization in food prices after Ramadan. While core indicators show a more balanced outlook, sticky service inflation (monthly increase of 2.39%) remains a key risk to monitor.

“So, what will the central bank do in light of this data? We expect the CBRT to skip the April 22 meeting and keep the policy rate unchanged at 37%. The bank will likely maintain its tight stance through liquidity management within the interest rate corridor,” he said.

What about the risks?

The epicenter remains the Middle East. Escalating rhetoric, threats, or actual targeting of infrastructure and energy facilities continue to weaken hopes for a ceasefire.

In markets driven heavily by developments, a cautious stance remains essential, while the BIST index is expected to move within the 12,400-13,400 range.

5 min read

5 min read