Newsletters

Newsletters

Central Bank of the Republic of Türkiye (CBRT) Governor Fatih Karahan reiterated Friday that the size of policy measures would be assessed prudently at each meeting based on the inflation outlook. "If there is a significant deviation from interim targets in the inflation outlook, the monetary policy stance will be tightened," he said.

His remarks came during a presentation in Istanbul titled "Monetary Policy and Inflation Outlook in Türkiye," where Karahan laid out the central bank’s approach amid signs that the pace of disinflation has moderated in recent months.

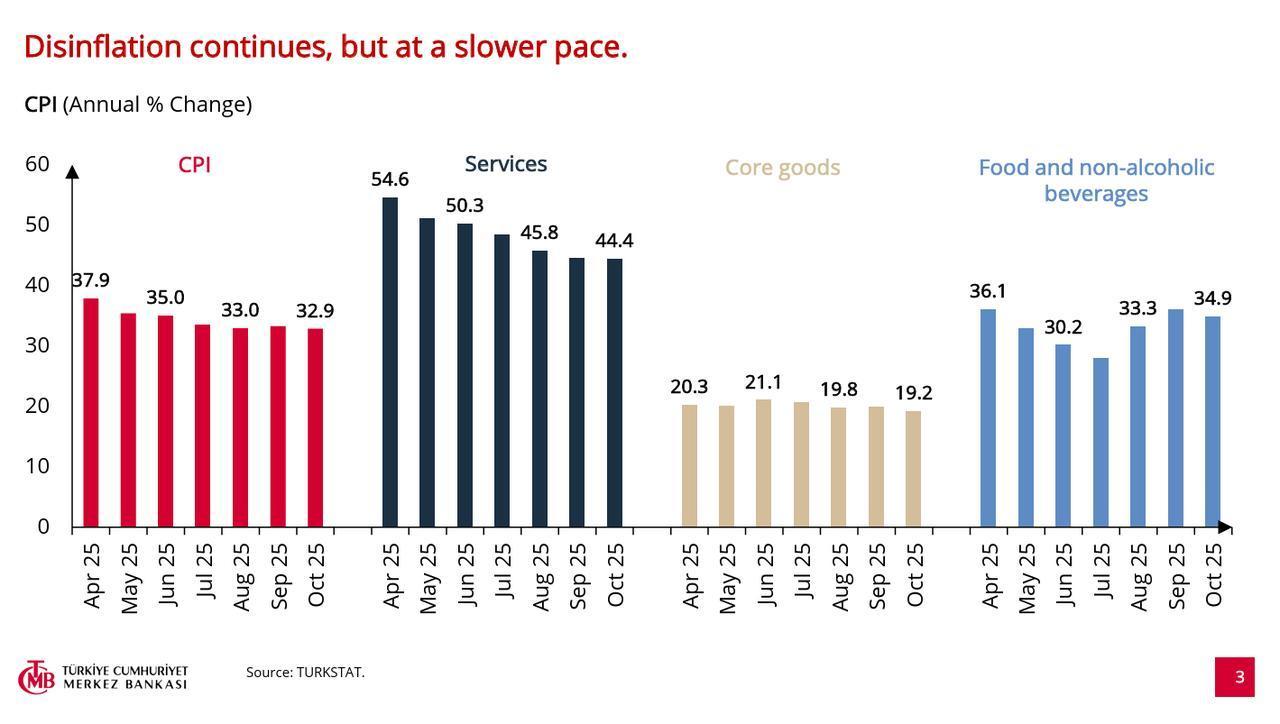

Karahan noted that the disinflation trend remains intact but is proceeding at a slower pace. Temporary upward pressures, such as adverse weather, have driven food prices higher, while strong seasonal factors continue to influence clothing prices. Rent inflation is showing signs of deceleration, but core indicators point to a slowdown in the downward trajectory of inflation.

Despite improvements in inflation expectations, Karahan emphasized that expectations remain high, although the range of responses in surveys is narrowing. He added that market pessimism has decreased and firms’ pricing behavior is improving.

Retail sales and credit card transactions are both reflecting a deceleration in consumer demand. While industrial production has declined slightly, services output has remained flat, contributing to signs of cooling in the broader economy. Labor market indicators, such as the composite labor conditions index, also show easing tightness.

Karahan also observed that some components tied to backward indexation are pulling headline inflation lower, while underlying disinflation momentum remains broadly intact.

The same day, the CBRT published the second edition of its semiannual Financial Stability Report, which reinforced the narrative that tight financial conditions are helping to rebalance domestic demand and support disinflation.

The report stated that credit growth remains in line with the disinflation path, with loan and deposit pricing adjusting to policy rate changes and expectations. Macroprudential tools have been used to slow foreign-currency loan expansion and strengthen the monetary transmission mechanism.

However, the report also pointed out that tighter financial conditions have begun to affect asset quality, with consumer loans performing worse than corporate lending.

Karahan, in the preface to the report, echoed the message that the tight policy stance is producing results in credit dynamics and expectations. He also noted that the use of foreign-exchange-protected deposit accounts has dropped sharply, with new account openings and renewals now halted.

The Financial Stability Report highlighted increased investor interest in Turkish lira assets following volatility in the first quarter of the year. The share of lira-denominated deposits has remained high and stable, and central bank reserves have improved.

Despite global uncertainty and geopolitical risks, Türkiye’s sovereign risk premium has continued to decline, which the report said has supported improved external financing conditions for both the banking sector and real economy. The banking system’s profitability, strong liquidity buffers, and capital adequacy also contributed to macro-financial stability.

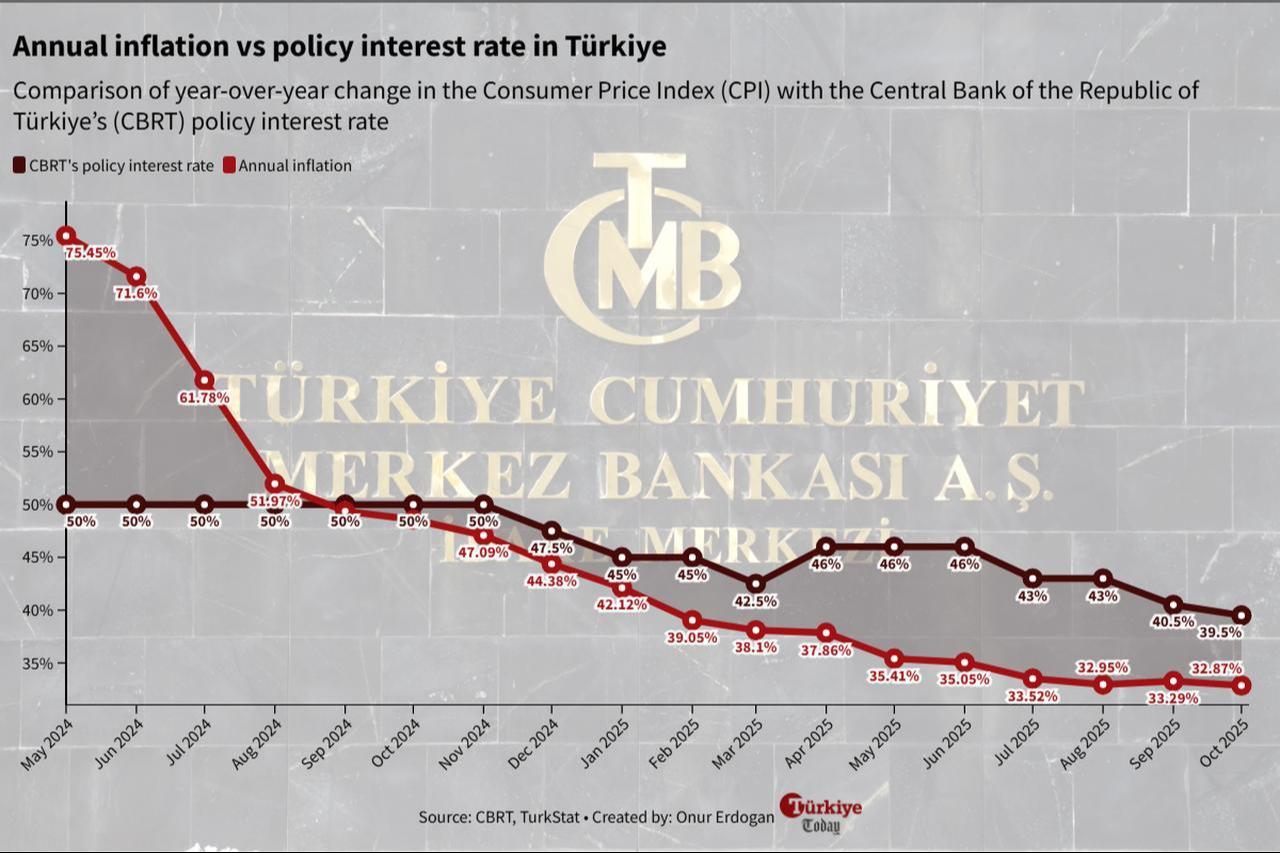

The Monetary Policy Committee is due to meet on Dec. 11 for its final interest rate decision of the year. Since July, the central bank has cut its policy rate from 46% to 39.5% over three consecutive meetings, although the size of the cuts was reduced to 100 basis points in October as disinflation began to slow.

According to the central bank’s November survey, market participants expect at least another 100 basis-point cut in December. However, the final decision may depend on November inflation figures, which are projected to rise by around 1.5% month-on-month.

ING Global estimates that Türkiye’s economy grew 3.8% year-on-year in the third quarter but flagged signs of slowing momentum across both supply and demand indicators. The Dutch lender forecasted a monthly inflation rate of 1.3% in November and an annual rate of 31.6%, down from 32.87% in October.

If inflation surprises to the downside, ING noted that expectations could shift toward a larger rate cut in the upcoming MPC meeting.

1 min read

1 min read

1 min read

1 min read