Newsletters

Newsletters

This article was originally written for Türkiye Today’s weekly economy newsletter, Turkish Economy in Brief, in its May 18 issue. Please make sure you are subscribed to the newsletter by clicking here.

Over 2.5 months have passed since the outbreak of the war in the Middle East, and the “fragile ceasefire” situation that began in early April has, for now, been preserved.

However, a permanent agreement has still not been reached.

The Strait of Hormuz, through which 20% of the world’s oil supply passes, remains closed.

Oil posted a weekly close above $100 for the third consecutive time. Brent crude finished last week near $110 per barrel, marking a sharp 9% weekly gain.

Alongside elevated oil prices, the U.S. 10-year Treasury yield climbed to its highest level since February 2025, testing 4.60%, while the dollar index moved toward 99.25 with a weekly gain approaching 1.5%.

In the U.S., the annual Consumer Price Index (CPI) came in at 3.8% in April and the Producer Price Index (PPI) at 6.0%, both exceeding forecasts and signaling serious risks.

In global markets, particularly in the U.S., the artificial intelligence-driven rally has given way to fears of high inflation and weak growth.

As markets confronted macroeconomic realities, notable sell-offs were seen not only in stock markets but also in metals such as gold, silver and copper. At this point, expectations for Federal Reserve rate cuts this year have nearly disappeared.

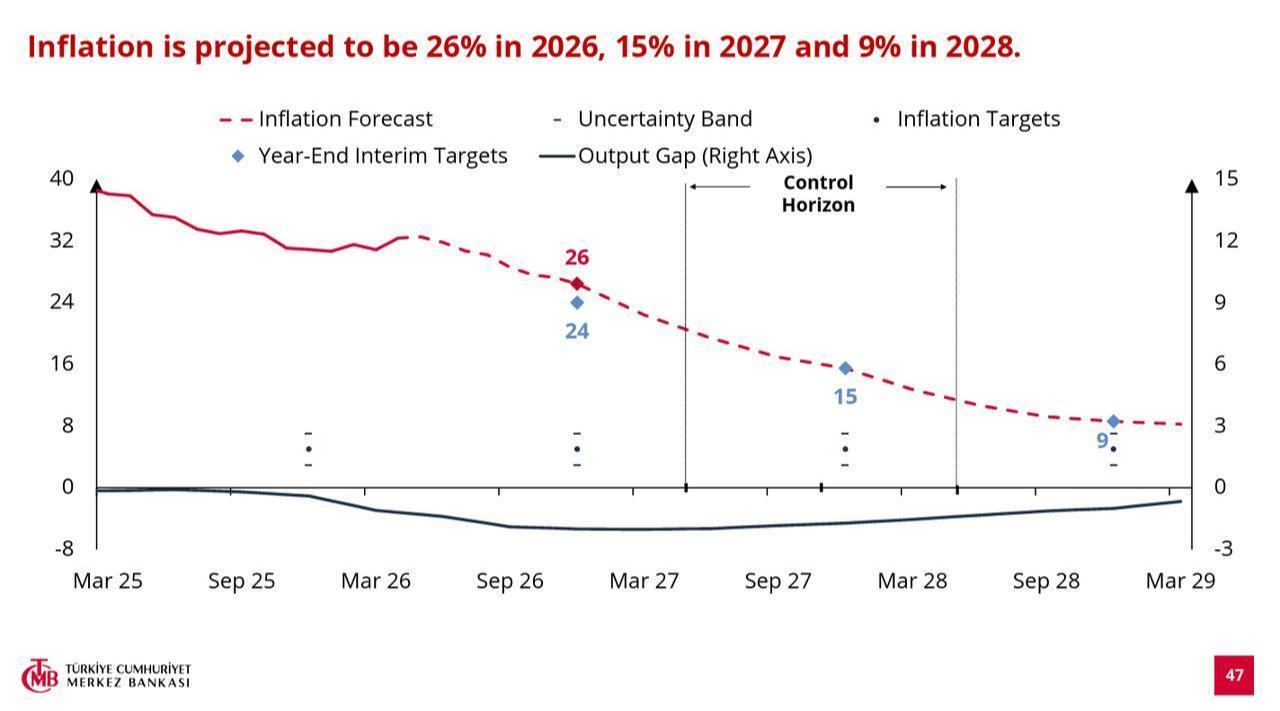

Against this backdrop, the Central Bank of the Republic of Türkiye (CBRT) released its second Inflation Report of 2026. The report is particularly important as it is the first inflation report published after the war began.

The CBRT revised its inflation forecasts upward because of rising geopolitical risks and higher energy prices. Accordingly:

CBRT Governor Fatih Karahan pointed to factors such as the course and intensity of the war, its potential impact on the inflation outlook, and the effects of economic cooling on inflation, stating:

“We believe the current stance in monetary policy remains appropriate until these uncertainties ease somewhat. From now on, all options are on the table. We will make decisions based on the inflation outlook at that time, as well as incoming data and news flow.”

Governor Karahan also noted that the CBRT paused policy rate adjustments on March 1 and, during this process, raised the funding rate by 300 basis points to 40%, the upper band of the interest rate corridor.

“We use the upper band more actively during periods of elevated risk. When this persists for a long time, we move toward normalization. Keeping the policy rate and funding rate this far apart for an extended period is not appropriate either in terms of communication or monetary policy implementation.”

He emphasized that future decisions will depend on whether uncertainties decline and in what direction.

Karahan said that while the costs of disinflation are discussed from time to time, inflation itself also imposes a very high cost.

He stressed that high inflation disrupts income distribution, prevents efficient allocation of economic resources, and negatively affects the economy’s potential growth. He also highlighted that savings tend to remain “under the mattress” in a high-inflation environment, while dollarization increases.

“We also see savings declining in a high-inflation environment, while appetite for consumption rises. Falling savings lead to high and chronic current account deficits. Therefore, our primary objective is to bring inflation down effectively to low levels.”

Following the report, Karahan reiterated during a business meeting in Konya that monetary policy would be tightened further “if a significant and persistent deterioration in the inflation outlook occurs.”

At this stage, expectations for tight monetary policy have increased not only for the CBRT but also for central banks globally. Questions about when rate cuts may begin are now being asked far more quietly.

However, reports released after the CBRT meeting drew attention to Is Yatirim’s forecasts. The institution expects the CBRT to leave rates unchanged at its first Monetary Policy Committee meeting on June 11.

According to its baseline scenario, in which the Strait of Hormuz reopens to tanker traffic in June, and oil prices stabilize above pre-war levels due to geopolitical risk premiums, funding is expected to gradually shift toward the policy rate level of 37% during July and August.

The analysis also projected three separate 100-basis-point rate cuts during the September, October, and December MPC meetings, with the year ending at a 34% policy rate.

In an assessment by Kuveyt Turk Yatırım, it was stated that the CBRT has moved toward a more cautious policy path and strengthened its guidance that tight monetary policy will be maintained for an extended period.

The report added:

“In the coming period, the course of energy prices, exchange-rate pass-through, and rigidity in inflation expectations will continue to be the main determining factors for the monetary policy outlook.”

Meanwhile, Borsa Istanbul’s benchmark BIST 100 index lost 4.6% last week amid prolonged uncertainty, closing at 14,367. Analysts point to 14,200 as a key support level, while the previous peak of 14,532 is now seen as resistance.

Current market conditions could improve only if an agreement is reached that would reopen the Strait of Hormuz and push oil prices back below $100.

7 min read

7 min read